Convincing evidence that three industries colluded to make the 1% wealthier at the expense of the 99%

The following provides specifics of an insidious cover-up that is depriving 99% of Canadians of a deserved $200 billion, and much more. For credibility, four top politicians have responded or acted based on the details below.

Premier Danielle Smith, who has received these details, justifiably demanded Alberta’s estimated $100 billion share of our $675 billion Canada Pension Plan (CPP) fund, as shown below.

Pierre Poilievre, in his email below, called the following recommendation “a new and innovative idea to rescue our economy.”

Finance Minister Freeland unsuccessfully attempted to refute my findings.

Finance Minister Morneau used my research, which uncovered a 76% Guaranteed Income Supplement (GIS) clawback to alter GIS legislation. Low-income seniors now receive $440 million more per year in GIS payments.

As a professor emeritus (Business), I have studied the CPP for eight years. The details below show that deserving Canadians are being subtly deprived of 450 times $440 million, $200 billion, and much more. It uncovers a cleverly concealed bribery scheme that is making the wealthiest 1% of Canadians even wealthier at the expense of the other 99%.

Because CPP Investments has been declared the best pension fund investor in the world, our CPP fund now has an irrefutable $400 billion surplus. Based on standard pension practice, roughly $200 billion should be distributed. Such a surplus distribution would give 20 million Canadians $10,000 each, increase our anemic GDP by 3%, increase business profits by 20%, reduce our deficit by $50 billion, help solve income inequality and much more.

However, the financial industry, the actuarial industry and the media industry would lose if the news of the CPP’s surplus became known. The evidence below is convincing that these three industries have rigged our capitalist system so that Canada’s wealthiest 1% can increase their wealth at the expense of the remaining 99%.

Several Experts and Icons Recommend Suspicion and Vigilance.

To make these disturbing allegations more credible, below are warnings from several prominent Canadians. They state that, under-the-radar, selfish powers are defying democracy so they can become even wealthier.

In her book, PLUTOCRATS, Finance Minister Chrystia Freeland highlights the prevalence of elite attempts to use political influence for personal gain, stating,

“In an age of super-wealth, we need to be constantly alerted to efforts by the elite to get rich by using their political muscle to increase their share of the pre-existing pie, rather than adding value to the economy and thus increasing the size of the pie overall.”

Mark Carney, candidate for Liberal leadership, echoes these concerns in his book VALUE(S), describing Canadians as victims of

"Twisted economics, an accompanying amoral culture, and degraded institutions whose lack of accountability and integrity accelerate the system’s dysfunction."

Pierre Poilievre asserts that "Our system is broken.” and “Fire the gatekeepers.", probably alluding to our complicit Chief Actuary and the complicit President of the CBC.

David Meslin, Canada's foremost expert on democracy, in his book "TEARDOWN," states,

“Our political system has evolved into a sophisticated enabler of mass institutionalized bribery... powerful corporations continue to wield enormous power in our legislatures.”

Duff Conacher of Democracywatch.ca emphasizes the significant financial impact of corporate cash, stating,

"Corporations spend $25 billion annually on their lobbying and promotion efforts."

If capitalism is so suspect, what specific companies or industries are “using their political muscle to increase their share of the pre-existing pie?”

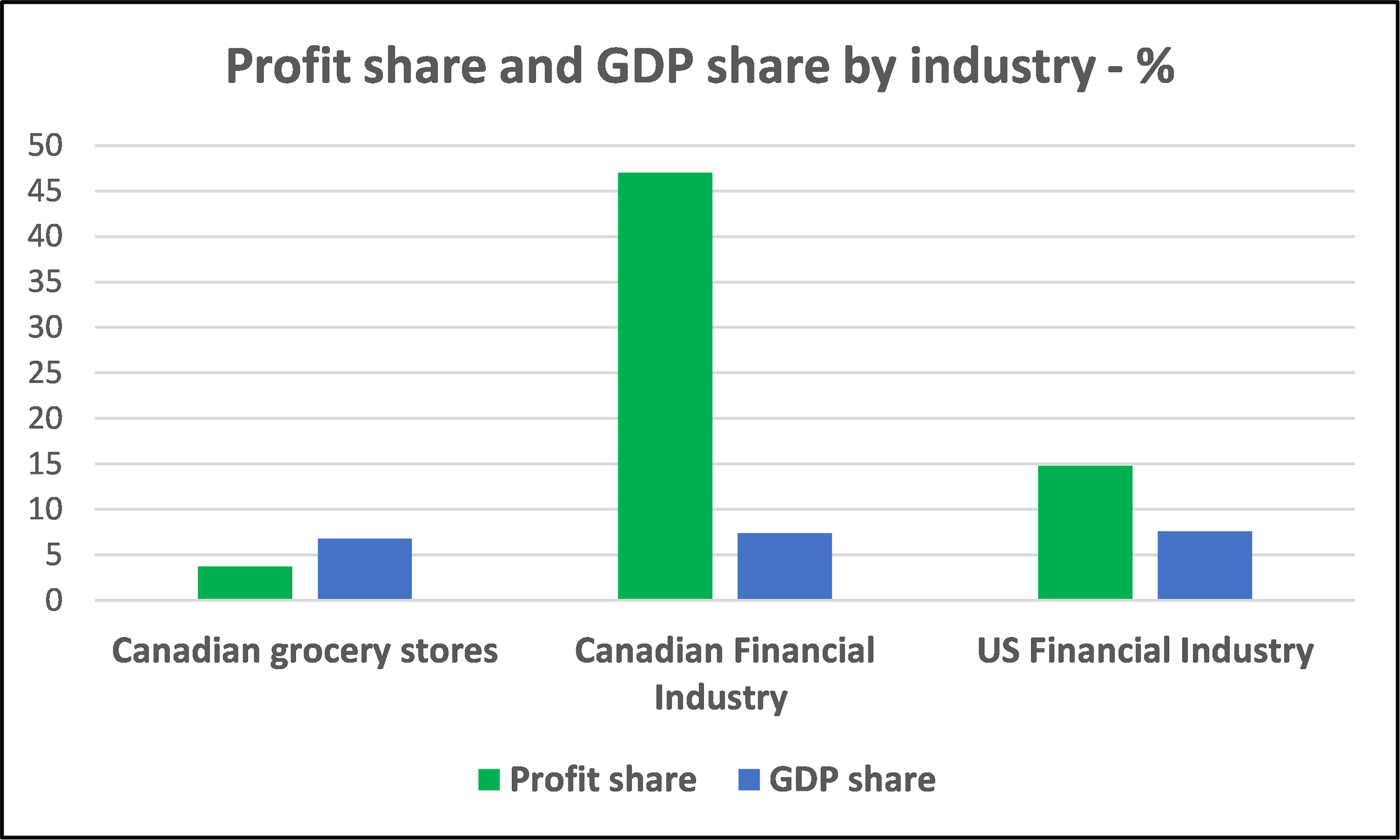

It is probably not those companies that provide goods or services. The law of supply and demand keeps them somewhat profitable. Walmart and Costco are excellent examples.

However, consider Canada’s mysterious financial industry. They earn 47% of all corporate profits in Canada but only contribute 7.4% to our anemic GDP. In 2020, their profit was a whopping $125 billion, aka $125,000 million. For comparison, the US financial industry only earns 17.3% of all corporate profits in the US.

The following shows how Canada’s financial industry has managed to “use their political muscle” to deprive millions of Canadians of billions of deserved dollars so that they can greedily continue collecting 47% of Canadian corporate profits.

Why our CPP has a huge surplus.

My second cousin, John MacNaughton, was CEO of CPP Investments from 1999 to 2004. Up until 1999, the fund was composed of mostly low risk bonds and guaranteed income certificates. John spearheaded a move to invest in riskier investments, including stocks, private equity, real estate, infrastructure and much more, worldwide. This change in investment strategy has generated very large profits for the 22 million members of the CPP, at very little risk. John’s initial investment strategy has resulted in CPP Investments being able to state in a recent Globe and Mail advertisement that they have had “the highest returns of any global pension fund. Period.”

In 2010, our Chief Actuary stated he needs a CPP fund value of $347 billion on January 1, 2025 in order to fund all pensions for 75 years. Thanks to the outstanding success of CPP Investments, the actual comparable fund value was an estimated $675 billion, meaning our CPP fund now has a surplus of roughly $303 billion. Moreover, if we forecast using CPP Investments’ 15-year return averaging 10%, as pension experts recommend, the surplus becomes $400 billion. This means our CPP fund is 338% of what is needed to fund all pensions for the next 75 years.

Aside from investment return, actuarial science calculates pension fund stability by forecasting for mortality, fertility, inflation, net migration, unemployment, participation, GDP and number of disability recipients. Since 2010, all these factors combined, over 12 years, have resulted in the fund now having $18 billion more than predicted. This is another reason that justifies declaring a surplus.

The left image shows that, in 2010, our Chief Actuary specified our CPP fund needed a value of $347 billion value on December 31, 2024 to fund all pensions for 75 years. The right image shows the actual fund value was $675 billion on September 30, 2024.

The left image expected an investment return averaging roughly 6.3% per year (in the large red box). Global SWF is a New York-based pension industry specialist. They recently analyzed all Public Pension Funds, worldwide. Below shows that CPP Investments, the best pension fund investor in the world, averaged a 10.9% return for the 10 years ending in 2022.

The power of compound interest is large. For example, investing $1,000 at our Chief Actuary’s specified 6.3% return yields $1,842 in 10 years. Investing $1,000 at CPP Investments’ 10.9% return yields $2,814 in 10 years, resulting in over two times the investment return.

Who owns this $400 billion surplus? Because CPP Investments used Canadians’ money to accumulate this return, based on standard pension practice, this surplus belongs to all contributors to the CPP.

How much would you receive from a surplus distribution? It depends on how much of your contributions were used to accumulate the surplus. For example, a younger Canadian, because he has contributed less, would receive less from the surplus. Conversely, a 55-year-old Canadian in 2010, when the surplus started accumulating, may have had $100,000 in the fund. He would receive much more.

CPP Investments is proud of their outstanding ability to invest our CPP contributions with success better than any other pension fund in the world. The following graph was recently published in various Canadian media, as a paid advertisement.

The graph below shows how our CPP fund has evolved from being perfectly balanced in 2010 to a $322 billion surplus today.

Forecasting using CPP Investments’ likely ongoing 10.9% return, as pension experts recommend, we only need roughly $200 billion in the fund today to meet all future commitments. This means the fund is 338% funded and has a $475 billion or 238% surplus. When a pension fund has a mere 25% surplus, a surplus distribution is recommended. That is why, in 2000, when the Ryerson University Pension Plan had a mere 18% surplus, the CRA demanded a surplus distribution. Professors, including me, received as much as $20,000 each.

Consider the benefits or a recommended $200 billion surplus distribution:

Twenty million Canadians would receive $10,000 each, on average,

Business profits would increase by 20%,

Our GDP would increase by roughly 6%, because of the multiplier effect ($200 billion is 6.7% of our GDP),

Employment would increase,

Charitable donations would increase,

Poverty would decrease,

Income inequality would decrease,

Our troubling deficit would decrease by roughly $50 billion, thanks to increased income tax and HST,

The 100,000 low-income seniors who will die this year could enjoy increased longevity and improved quality of life with their deserved $10,000,

CPP Investments could sell off its poorly performing investments, thereby increasing its overall return to 15%, for example,

Several other positive outcomes.

No actuary, economist, politician, or journalist has provided one reason to NOT distribute the CPP’s surplus.

Still more benefits

We all have a personal fund within the CPP’s giant fund. Presuming a 10.9% return, consider a 25-year-old earning, for example, $50,000 today. Here is how his personal fund would grow.

With $3.2 million in his personal fund at age 65, presuming an ongoing 10.9% return, using the investment income only, he could enjoy a $350,000 CPP pension. He could leave the principal of $3.2 million for an emergency or for his family when he passes on.

What about inflation? Based on a 2% inflation rate over 40 years, $350,000 becomes $160,000 in 2025 dollars. Based on a 3% inflation rate over 40 years, $350,000 becomes $107,000 in 2025 dollars.

(For advanced analysts, this analysis accounts for the fact the CPP is a pay-as-you-go pension plan and presumes the CPP’s $400 billion surplus will be distributed today.)

Ongoing high returns for CPP Investments are probable. They have many investment advantages over the average investor. For example, their private equity investments, constituting one-third of their $675 billion portfolio, recently achieved an unprecedented 33.2% return, as shown in their Annual Report 2022 (Page 43).

Why the Financial Industry has spent millions to suppress the news of the CPP’s surplus

One would naturally think, as I did six years ago, that the financial industry would want these numerous, considerable benefits reaching millions of Canadians and our sputtering economy. However, the reverse is true. The following explains why.

The financial industry recommends Canadians invest 15% of their income towards retirement. Canadians are listening. We now have $4 trillion invested in RRSPs and TFSAs alone. This is $100,000, on average, for each of 40 million Canadians. At an estimated 1% charge for investment advice, the financial industry earns $40 billion per year on RRSPs and TFSAs alone. Because there are maximums on RRSP and TFSA accounts, Canadians may have an estimated second $4 trillion also invested with the financial industry.

It was probably intense lobbying by the financial industry that led to the developments in of RRSPs and TFSAs'. They tax avoidance investment alternatives have provided a win/win for both Canadians and our financial industry, in the short run. However, Canadians will eventually pay because these policies have resulted in a large decline in tax collection, thereby contributing to our spiraling debt.

Conversely, the news of the CPP’s surplus would lead to a win/lose for Canadians and our financial industry. Not only is there zero lobbying for a CPP surplus distribution, three greedy industries have colluded to conceal the most newsworthy, most impactful story in Canada in years.

However, if young Canadians knew a $100,000 in 2025 dollars CPP pension likely awaits them, their desire to invest 15% of their income towards retirement would plummet. Many, now struggling financially, would use their additional 15% in income to improve their quality of life today. The financial industry would then lose billions of dollars in investment fees, annually. Moreover, some Canadians might even cash in their RRSPs and TFSAs now, instead of waiting until age 65.

Moreover, when a member of the CPP dies, his surviving spouse receives a pension that is roughly 60% of her partner’s pension. With a probable $100,000 CPP pension at age 65, and a portion of a spouse’s pension available, life insurance becomes unnecessary, resulting in a big decline in a second moneymaker in the financial industry.

The Case for Voluntary Contributions to CPP Investments

The financial industry has a multibillion dollar reason to fear the idea of voluntary contributions to CPP Investments - they cannot compete. The idea is not outlandish—Canada's former Finance Minister, Jim Flaherty, explored this concept in 2011. However, he faced a deluge of misinformation and relentless lobbying from the financial sector, which derailed the initiative. Sadly, Mr. Flaherty, likely one of the few Finance Ministers capable of challenging the powerful financial industry, passed away in 2014 at just 64 years old.

Looking ahead, there is hope for reform. In January 2025, Pierre Poilievre, with his firm stance of "never listening to lobbyists," could soon legislate voluntary contributions. This is an idea that would resonate with the vast majority of Canadians, as explained below.

The Astonishing Power of Compound Interest

Compound interest, described as one of the most powerful forces in finance, is a concept that even Albert Einstein reportedly praised:

"Compound interest is the eighth wonder of the world. He who understands it, earns it; he who doesn’t, pays it."

To understand how voluntary contributions to CPP Investments and compound interest could benefit Canadians, consider the case of a 25-year-old who aims for a retirement income of $50,000 per year (indexed), beginning at age 65 and lasting through his expected lifespan to age 85.

Two Investment Scenarios

Self-Investing:

Following the financial industry’s common recommendation of a 60/40 portfolio split (60% equities, 40% fixed income), the investor might expect an average annual return of 4.4% after fees.

To achieve his goal, the individual would need to contribute $6,000 per year over 40 years, $240,000 in total, to collect $1 million over 20 years in retirement.

Few 25-year-old Canadians can contribute an extra $6,000 without seriously hampering their quality of life.

2. Voluntary Contributions to CPP Investments:

CPP Investments has averaged a 10% annual return for 15 years. This outstanding return will likely continue.

Under this scenario, the individual would only need to contribute $1,000 per year over 40 years, $40,000 in total, to collect the same $1 million over 20 years in retirement.

Because of the potential benefits, most 25-year-olds would make the slight $1,000 per year sacrifice because of the huge benefits available.

The difference is staggering: by utilizing CPP Investments, the investor requires just one-sixth of the annual contribution to achieve the same outcome.

The Impact Over Time

The graph below illustrates the dramatic difference in portfolio growth between these two approaches.

By leveraging a Tax-Free Savings Account (TFSA), the $50,000 annual retirement income would be tax-free. However, inflation would reduce its future buying power to roughly $23,000 in today’s dollars. Supplementary income sources, such as Old Age Security (OAS) of approximately $9,000 per year and up to $23,000 from the CPP, would bring his total tax-free income at age 65 to roughly $50,000 annually, in 2025 dollars.

The Stark Contrast

This comparison reveals a stark difference:

Self-investing requires six times the contributions of investing through CPP Investments.

Voluntary contributions could enable Canadians to achieve the same retirement income with far less effort and financial burden.

This explains why, in 2016, when Finance Minister Bill Morneau announced modest CPP changes, Janet Ecker of the Toronto Financial Services Alliance expressed relief. She feared significant CPP reforms like voluntary contributions could:

"Undermine a lot of successful, legitimate, (retirement savings) products in the investment industry."

But who should be “undermined”?

Should it be an industry that captures 47% of all Canadian corporate profits, largely for its own benefit?

Or should it be the millions of Canadians struggling to save for retirement?

A Personal Example

Consider three university associates who joined the financial industry after graduation. Their wealth is now estimated at $100 million each. Meanwhile, ordinary Canadians are left to navigate the financial industry’s high fees and subpar returns, coupled with a pathetic, deceptive Chief Actuary to watch over our CPP contributions, 10% of our earnings, lifetime.

Could CPP Investments handle Voluntary Contributions?

If Canadians could contribute up to $1,000 annually to CPP Investments, the program would not be overwhelmed. For example, if 10 million Canadians opted for the maximum contribution, the total investment would be $10 billion per year—a manageable figure for a fund now valued at roughly $700 billion.

Moreover, the CPP currently holds a $400 billion surplus, of which $200 billion should be distributed under standard pension practices. Allowing voluntary contributions would provide CPP Investments with additional capital to offset a deserved CPP surplus distribution.

Conclusion

The financial industry cannot compete with CPP Investments’ proven track record of 10% annual returns. Voluntary contributions would give Canadians six times the value compared to traditional investment options. If made available, voluntary contributions would likely become a transformative solution for Canada’s retirement system, empowering millions while challenging the dominance of the financial sector. It would also substantially reduce skyrocketing Guaranteed Income Supplement (GIS) payments.

Canadians Deserve Better: The Case for Voluntary Contributions to CPP Investments

By coincidence, our CPP gives us the same return on our contributions as self-investing does - 4.4%. With as much as $7,500 contributed in 2025, if our contributions directly received CPP Investments’ 10% return, a 25-year-old would have a $375,000 CPP pension in 40 years, equivalent to a $169,000 pension in 2025 dollars. If we transformed the CPP into a Defined Contribution (DC) plan instead of a Defined Benefit (DB) plan, Canadians would receive six times the CPP pension.

Because of our Chief Actuary’s failure to acknowledge the CPP’s $400 billion surplus, Canadians will continue to receive a 4.4% return on their contributions. Meanwhile, CPP Investments will continue to use their contributions to achieve a 10% return.

A Hybrid Model: The Best of Both Worlds

A compromise is possible:

For example, half of contributions could be treated as DC, likely yielding a $85,000 pension (in 2025 dollars) in retirement for young Canadians.

The other half of contributions would be more than enough to meet current pension promises. They could remain in the DB system.

Younger Canadians are now struggling with anxiety and depression. As they , watch their contributions grow exponentially, they would no longer feel pressured by the financial industry’s ominous warnings:

"Invest 15% of your income for retirement—or face poverty in old age."

Instead, they could enjoy as much as 15% more income today, with greater peace of mind, anticipating a likely $85,000 CPP pension (in 2025 dollars).

A Government Agency That Excels

Most Canadians agree that some essential services are most effective when overseen by the government. For instance, Universal Healthcare, The Military, and Education are probably all more effective because our government oversees them. However, government agencies often have a reputation for inefficiency, high costs, bureaucratic red tape, inconsistent goals, and poor service delivery.

In Canada’s history, have any government agencies achieved the level of success demonstrated by CPP Investments, widely regarded as the best pension fund investor in the world? Its stellar performance raises an important question:

Why can’t Canadians benefit directly from this one government agency that excels? Why must we contribute six times as much elsewhere to achieve the same retirement income CPP Investments could give us?

This failure has had devastating consequences: one million low-income seniors have died prematurely over the past decade, living shorter lives of reduced quality. Meanwhile, Canadians continue to see returns of just 4.4% on their CPP contributions, despite the outstanding 10% investment performance of CPP Investments.

Confronting Industry Greed

Canadians should not continue to subsidize an industry that prioritizes its profits over their well-being. It’s time to combat this greed and demand better. Any politician who opposes voluntary contributions to CPP Investments owes Canadians an explanation. If they cannot provide one—and even Finance Minister Chrystia Freeland has attempted and failed to do so—then they must acknowledge their allegiance to the financial and actuarial industries over the millions of struggling Canadians they are supposed to democratically represent.

The CPP’s surplus can help solve many other serious problems

Mental health has emerged as a big problem among Canada’s youth. Surveys indicate many fret about retirement security. The revelation that a $100,000 CPP pension likely awaits them, coupled with as much as 15% more income available today, could help bring peace of mind to millions of young, anxious, struggling Canadians. For some, this 15% increase in income could even pave the way for a down payment on a home.

Canada’s sputtering economy would also improve. If Canadians had as much as 15% more income available to spend, and they received a surplus payment of $10,000, our anemic GDP and business profits would increase substantially, resulting in more income tax and HST revenue. The problems of our spiraling deficit and sluggish GDP would then be substantially addressed.

Old Age Security (OAS) and the Guaranteed Income Supplement (GIS) now cost our federal government a whopping $78 billion per year, 17% of all federal expenses. They are scheduled to skyrocket at a rate of 5% per year to 2035. If most Canadians eventually receive a $100,000 CPP pension in 2025 dollars, this mushrooming expenditure could decline considerably.

Finally, expensive contributions to other pension plans could stop. Currently employees contribute as much as $10,000 per year per employee, matched by the employer, towards a pension plan. With the CPP likely providing a $100,000 pension, this cost to both employees and employers could be reduced substantially.

How could so many benefits not reach struggling Canadians?

The above shows that the financial industry has the motivation to suppress the news of the CPP’s surplus. The news could likely result in billions of dollars in lost profit, per year. But do they have the resources? Absolutely. In 2020, for example, they earned a massive $125 billion in profit. For clarification, most Canadians understand $1 million is big. The financial industry earns 125,000 times $1 million every year.

The evidence below is convincing that the financial industry has invested, for example, a mere 1% of their profit, a very convincing $1.25 billion to subtly and illegally suppress the news of the CPP’s surplus. They have done this so that they can continue to collect huge profits from millions of Canadians who have been duped into thinking they need to invest substantially now or experience a retirement in poverty.

The wealthy already have advantages

Few Canadians realize that, in the 1960’s, the top tax rate in Canada and the US was over 90%. Then, likely using bribery, the wealthy managed to decrease that rate to roughly 53% in Canada and 40% in the US.

Moreover, in Canada, 47 of 51 tax loopholes favour the rich. The wealthy already have huge advantages. This insidious CPP surplus cover-up, orchestrated by the greedy wealthy, needs to be stopped.

On this crucial issue, Democracy has vanished

Democracy expert David Meslin’s statement in his book "TEARDOWN: Rebuilding Democracy from the Ground Up” is telling. He wrote:

“Our political system has evolved into a sophisticated enabler of mass institutionalized bribery... powerful corporations continue to wield enormous power in our legislatures.”

Even the NDP could potentially secure a landslide majority by merely promising to give $10,000 to each of 20 million Canadians, let alone the other benefits alluded to earlier. So, why haven't they? Did the financial industry strike this example bargain with all three political parties:

"If you never mention the CPP’s surplus, we will give your party $50 million per year"?

This would explain why all politicians remain mute regarding the CPP’s surplus, even though all 334 MPs have received these details, twice, in the last five years. They all act as if they have signed some NDA that silences any discussion of the CPP’s surplus. Only Mr. Poilievre, who has stated “Our system is broken.” and “Fire the gatekeepers.” has responded, as shown below. My principled MP, Jane Philpott, upon learning of these details, stated “Disgraceful lobbyists.”

Alberta Premier Danielle Smith wants no part of this bribery. She has demanded Alberta receive its fair share of our CPP fund so that she can give Albertans the numerous benefits described above.

The Canadian Media is Obviously Complicit.

Consider the landscape of our Canadian media over the past two decades. Can you recall a story more significant and impactful for Canadians than the following:

"Adhering to standard pension practice, the CPP should now distribute $200 billion of its $400 billion surplus to deserving Canadians, with no risk to future CPP pensions. The potential benefits are vast, including 17 million Canadians receiving $10,000 each, a 20% increase in business profits, a 3% GDP boost, heightened employment, reduced poverty, reduced income inequality, a deficit reduction of $50 billion, and much more.

Because CPP Investments has many advantages over the average investor, it is likely they will continue investing so successfully. If so, an average 25-year-old could have a $100,000 CPP pension in 2025 dollars. This means he can stop investing now towards retirement and use his additional income to improve his current quality of life."

If such a story were published, politicians would be forced by protesting Canadians to legislate CPP changes so that millions of Canadians and our anemic Canadian economy could receive these benefits.

Canadians are starved for good news. After first struggling with Covid, most are now faced with high housing costs, unemployment, galloping inflation, mushrooming income inequality, climate change, crippling tariffs, and much more. It is criminal to deprive them of a deserved $10,000 and a virtually guaranteed high-income retirement.

Surprisingly, not one word on the CPP’s surplus has ever been published in Canada’s mainstream media. In contrast, in 2019, The Economist, the esteemed and unbiased international publication, stated:

"Canada’s vast pension fund is gaining even more financial clout. The fund’s portfolio size has more than tripled over the past decade and is going to become only more gigantic.”

Moreover, since those words were published, our "gigantic" CPP fund has expanded by another $300 billion.

Candid insights from Canadian media experts underscore the prevalence of bribery in the industry. John Miller, previously Managing Editor of the Toronto Star and Chair of Journalism at Ryerson University (aka TMU) has stated:

"The Canadian media is cannibalistic...They’re chewing away bone marrow of their own properties in order to make them a profit, so the whole public service aspect of journalism has taken a back seat. The overall quality of journalism has been lost."

Ex-world class journalist, Chrystia Freeland’s thoughts from her book PLUTOCRATS: The Rise of the New Global Super-Rich and the Fall of Everyone Else are:

"The super-rich have bankrolled a network of conservative think tanks, elite journals, and mass media outlets to dominate the debate over economic policy."

Mark Edge, Canadian journalist, academic and author. stated:

"Media owners don’t really care too much about journalism. It’s just a means to an end, and that end, of course, is making money."

Pierre Poilievre, likely Canada’s next Prime Minister, recently stated:

“We can’t count on the media to communicate our messages to Canadians. We have to go around them and their biased coverage.”

Mr. Poilievre constantly uses unbiased media like Youtube to convey his message to Canadians. He seldom speaks to the deceptive mainstream media.

The lengthy tentacles of the financial industry have even reached “our” CBC. Despite repeated submissions and shaming by me, executives at “our” CBC refuse to publish one word on the CPP’s surplus. This failure strongly justifies Mr. Poilievre’s threat to “Defund the CBC.” and “Fire the gatekeepers.”, probably alluding to the disgraceful president of the CBC.

Consider the ArriveCan APP. Our Canadian media has published an estimated 1,000 stories regarding this $60 million scandal. Meanwhile, our Canadian media has published zero stories on a scandal that is costing Canadians $200 billion, over 3,000 times the cost of the ArriveCan scandal. This further confirms media experts’ claim that our media has abandoned integrity for profit.

Instead of this highly impactful CPP surplus story, our media supplies us with a steady diet of stories that, financially, have virtually no impact on our day-to-day lives. The ArriveCan APP, the carbon tax, and foreign interference are the somewhat irrelevant stories that the media continued to bombard us with in 2024. Please compare any abuse you have personally encountered from these “scandals” compared to the abuse you are experiencing because you, and millions of other Canadians, are not receiving the CPP benefits described above.

The entire Canadian media, grappling to turn a profit, is controlled by a handful of questionable corporations, mostly within the financial industry. Did the financial industry orchestrate this example arrangement with all media owners?

“If you never mention the CPP’s surplus, we will give your company $50 million per year."

Appallingly, the few ethical journalists who have fought for this CPP surplus story are no longer employed. It appears that media owners will fire any journalists who have a conscience.

Compared to the US, most Canadians think we have a democratic country with an unbiased media that publishes all stories that are newsworthy. Because our media has collectively agreed to veto stories like the CPP’s surplus, our media is arguably worse than the US media.

The U.S. media landscape, with outlets like right-leaning FOX and left-leaning CNN, regularly presents opposing viewpoints, allowing citizens to consider multiple perspectives on critical issues. For example, a story as significant as Canada’s $400 billion CPP surplus (equivalent to $4 trillion in the US) would likely be published freely and then analyzed in depth in the U.S.

Actuaries Also Have Much to Lose.

If Canadians knew the CPP will likely give them as much as a $100,000 pension in 2025 dollars, few would contribute to any other pension plan. Then the need for actuaries, the watchdogs of pension plans, would plummet. This explains why the ten top Canadian actuaries who I have consulted have all denied the CPP’s $400 billion surplus with vacuous arguments.

Canada’s Chief Actuary oversees 10% of the lifetime earnings of most Canadians, totaling trillions of dollars. However, he operates without oversight. There are three oversight options that, on behalf of millions of Canadians, could check on the reporting of our Chief Actuary.

The Canada Revenue Agency. With jurisdiction over some pension funds, the CRA ordered the Ryerson University Pension Plan to distribute their 18% surplus. In 2000, professors, including me, received as much as $20,000 each.

Canada’s Auditor General. They audit most government organizations for fraud, mishandling of funds, inaccurate reporting and injustice to Canadians.

A CPP Board of Governors. Pension experts claim the success of every pension fund depends on a representative Board of Governors, composed primarily of contributors and pensioners. Actuaries report to them. The Board decides on investment policies, surplus payments, pension payments and contribution amounts. (CPP Investments has a very competent Board of Governors but their mandate involves investment decisions only.)

Regrettably, our Chief Actuary is not subject to scrutiny from any of these organizations. He has full control. An email to me from Finance Minister Chrystia Freeland shows she has little comprehension regarding our CPP. Meanwhile, one top Canadian actuary with a conscience stated, with disgust:

“Our Chief Actuary has done what pension actuaries frequently do - invent measures that are easily manipulated so that actuaries can control the narrative and hide things at will...I must remain anonymous because I am not allowed to criticize my fellow actuaries.”

Based on my eight years of research, after poring through thousands of pages of reports prepared by our Chief Actuary, I heartily concur with this disgraceful assessment.

Despite this undisputable CPP surplus, our Chief Actuary has stated to me, "The CPP is not in surplus" and “No further comment.”. Moreover, in thousands of pages of his reporting, he never mentions “surplus” even though our CPP now has a $400 billion surplus. Our Chief Actuary is supposed to serve Canadians with accuracy and honesty. Instead, he has chosen to deceive us so that he can protect his fellow actuaries in his at-risk industry.

Years ago, most Canadians paid with cash. When we gave a cashier a $20 bill for something costing $16.50, most of us scrutinized the change returned for accuracy. Meanwhile, as we all contribute 12% of our income to the CPP, we wrongly presume it is being handled with appropriate care, never suspecting three industries would greedily collude to conceal a $400 billion surplus that belongs to us.

Malcolm Hamilton, an actuary, is one of Canada’s foremost experts on pensions. He is associated with the C.D. Howe Institute, a think tank that will not reveal who funds them. Even though Malcolm could probably command $1,000 per hour as a consultant, he curiously spent 40 hours trying to convince me the CPP has no surplus. He failed miserably, using ridiculous arguments.

The disgraceful C.D. Howe Institute, probably funded by the financial industry, irresponsibly published a misinformation paper that suggests our CPP pensions are in jeopardy!

Did the Canadian Institute of Actuaries recently hold this meeting?

“Good day, fellow actuaries, from your President,

We cannot let Canadians know that CPP Investments’ will likely continue investing so successfully. Combined with the current $400 billion surplus, continued investment success means future CPP pensions will be so large that most Canadians will stop contributing to any other pension plan. A $100,000 CPP pension in 2025 dollars is probable for a 25-year-old. If Canadians know this, there will be a huge decline in the demand for other pension funds, and hence actuaries. We must act now to protect our at-risk industry.

Unfortunately, Professor Macnaughton’s CPP surplus analysis has obviously reached Premier Smith of Alberta. Her Alberta Pension Plan website boasts a surplus payment to seniors of as much as $10,000 each if Alberta receives their share of the $675 billion CPP fund. It also suggests Albertans and their employer will enjoy a $1,425 contribution reduction per employee per year.

Soon, citizens and businesses from other provinces will be saying,

‘If Albertans are scheduled to receive $10,000 each and a $1,425 contribution reduction per year, what about my province and me?’

Then complicit premiers will be forced to listen. The entire CPP surplus story will then be impossible to suppress, especially with the threat of social media looming.

Upon learning of the CPP’s surplus, Premier Smith probably asked the federal Liberals for a Canada-wide CPP surplus distribution. Thanks to the bribes by our friends in the financial industry, the Liberals refused. Then Premier Smith demanded Alberta’s share of the surplus, which is her right. She hired our actuarial friends at Lifeworks to determine how much Alberta deserves.

Here is a crucial question that must be now answered: How can we continue to keep this inconvenient news of the CPP’s surplus suppressed? We need to think outside the box.”

After many hours of thinking outside the box, members of the Institute presented a risky but effective strategy as follows:

“Even before her CPP request, our media has portrayed Premier Smith as an unhinged, un-Canadian, uncooperative premier who couldn't care less about the rest of Canada as long as Albertans benefit. We can use this portrayal to our advantage. There is an obscure clause in The Canada Pension Plan Act that, if taken verbatim, lets Lifeworks theoretically suggest Alberta deserves an outlandish 53% of the CPP’s $675 billion fund. It will slightly tarnish Canadians’ opinion of Lifeworks and actuaries but we must risk it. Actuarial science is so complex that few people will question it, especially since we are only following The Canada Pension Plan Act.

If we can get our friends controlling the media to attribute this ridiculous 53% claim to Premier Smith and not Lifeworks, Albertans and all Canadians will presume she is unhinged and all statements she makes regarding the CPP and its surplus should be ignored.

Canada’s media owners, thanks to cash from the financial industry, have never mentioned the CPP’s surplus, even though it may be the most newsworthy story in Canada in years. They can now skillfully cooperate and mislead the public into thinking Premier Smith, not Lifeworks’ actuaries, greedily claims 53% of the CPP fund.”

And the media did cooperate, as shown below.

The actuarial deception is ongoing. In the Fall of 2024, our Chief Actuary was asked to report her version of Alberta’s share of the fund. She refused. To further delay Alberta receiving its share of the fund, she may eventually shortchange Alberta, resulting in Premier Smith forced to consult Canada’s Supreme Court. This could take many years.

Alberta should only leave the CPP if they can still invest their share of the fund with CPP Investments, the best pension fund investor in the world. For example, the OMERS pension fund invests for 1,000 employers. For CPP Investments, subdividing the fund to represent ten provinces would be simple. Then each province could use their surplus share to help their own province. For a province to start their own investment organization would be pension suicide, as history has shown.

A much better solution would involve our likely next Prime Minister, Mr. Poilievre, legislating a Canada-wide CPP surplus distribution.

Democracy - traded in for cash?

There are only 45,000 financial analysts and actuaries in Canada, constituting just over 0.1% of our population. It is likely that the remaining 99.9% of Canadians, if informed, would overwhelmingly support a no-risk CPP surplus distribution of $200 billion. However, all three political parties refuse to propose or even discuss such a distribution. The democratic principles in Canada seem to have been abandoned. Instead of:

“Government of the people, by the people, for the people,"

Canadians are receiving:

"Government of the people, by the financial industry, for the financial industry."

Our suspect media, experiencing a shortage of topics, is currently dwelling on foreign interference on our democracy. Our media should focus more on domestic interference, right here in Canada. It is probably having 1,000 times the impact on the day-to-day lives of struggling Canadians.

The following is a stretch but it should be mentioned. Did the NDP, in a state of desperation, threaten to offer a CPP surplus distribution to all Canadians? Is it plausible that our Liberal government, possibly influenced by prodding from the financial industry, proposed a strategy of appeasement by forming the 2024 Liberal/NDP coalition? This coalition has provided dental care for children in low-income families and some Pharmacare. Canadians would probably prefer a $200 billion CPP surplus distribution over limited dental care and Pharmacare. However, we don’t get a choice.

Every year, thousands more Canadians’ lives are being shortened

There are two million Canadian seniors now living near the poverty line of $22,000 in income per year. Two thirds are women. An additional $10,000, similar to a 40% raise, could vastly improve their quality of life and longevity. Please recall that it was their money, and yours, that was used by CPP Investments to create this gigantic surplus.

Consider the plight of those 100,000 suffering low-income Canadian seniors expected to pass on in the next 12 months. Struggling to survive on an income near the poverty line, they can barely pay for rent and day-to-day living expenses. An additional $10,000 from the CPP’s surplus would lead to a substantially improved quality of life and a longer life. They could, for example, travel, dine out, buy a car, visit grandchildren, visit Florida, play golf, and enjoy all the other activities wealthier retirees take for granted.

One study shows that those seniors in the top quintile of income live 13 years longer than those in the bottom quintile. Tragically, the lives of these suffering seniors are being cut short because of the greed of millionaires in the financial industry. Intentionally shortening the lives of thousands of people is called genocide.

What about the benefits of an extra $1,000 to a low-income senior as opposed to a banker? The Economist recently wrote,

“The marginal benefit of an extra $1,000 is greater for the poor than the rich. A hungry family might buy food for a month; a banker might blow that amount on a single dinner, not including the wine.”

Next year, another 100,000 struggling seniors will die earlier than they should. Since 2016, roughly one million low-income seniors have died earlier than they should, with a lower quality of life. Please help stop this cover-up. Suggestions are below.

There are also 200,000 middle-income and high-income Canadians who will also die this year, never receiving their deserved surplus payment, which is closer to $15,000 each.

Generational equity, or fairness to all, is the primary goal of all pension fund managers. Disgracefully, our Chief Actuary has ignored this multibillion dollar responsibility to protect her at-risk industry and the financial industry.

Bank presidents are the most guilty…and could easily stop this cover-up

Banks oversee 70% of the $10 trillion in total financial assets in Canada. The bank presidents in the five big Canadian banks are each paid roughly $15 million per year to keep their profits flowing. Arguably, they represent 70% of the financial industry. If they agreed, one phone call to our politicians saying,

“The jig is up. Forget the bribes. Let’s release the CPP’s surplus. Our banks’ image (and my legacy reputation) are too much at risk.”

Because they refuse to use their power and influence to cancel this cover-up, they are guilty of depriving millions of struggling Canadians of the benefits listed above. This is a complete contradiction of their declared mandate. For example, TD bank’s slogan is “Enriching the lives of those we serve.”. A more accurate slogan is “Worsening the lives of those we serve.”

These organizations are also guilty

The tentacles of the greedy financial industry are ubiquitous. Canada's two foremost seniors' advocacy groups, CARP and CANAGE, have a mission statement that claims they will advocate vigorously for the well-being of seniors. For example, CARP’s stated mandate is to "Promote and protect the interests, rights, and quality of life for Canadians as we age."

However, both CARP and CANAGE, despite receiving repeated CPP surplus details from me, have not responded. Of a $200 billion CPP surplus distribution, seniors would receive $60 billion. As Canada’s only influential advocate for seniors, this failure to respond is especially suspicious because CARP and I partnered to secure an additional $440 million per year in GIS payments for low-income seniors. This failure to meet their mandate is probably caused by substantial "donations'' received from the financial industry. The agreement may have been worded as, for example,

“We will donate $10 million to your organization on the condition that you never mention the CPP’s surplus.”

Our CRA frowns on nonprofits like CARP that receive income from the public but do not match their advertised mandate. The CRA has been notified.

Eight years ago, I viewed think tanks with great respect. I thought they were packed with ethical experts who advise naive politicians regarding the best legislation for Canadians and Canada. However, think tanks are also curiously mute on the CPP’s surplus. Three facts confirm that they are a well-disguised scam:

Several think tanks have received the above details and never mentioned the CPP’s surplus. Instead, some have even written papers claiming our CPP pensions may be in jeopardy.

Malcolm Hamilton, the high-level actuary who suspiciously spent 40 hours trying to convince me there is no surplus, is associated with the C. D. Howe Institute, a think tank that refuses to reveal who funds them.

Canadians have no idea who funds these think tanks. Those Canadian think tanks that write about financial issues have all received an underwhelming rating between zero and two, out of 5, for revealing who funds them. The evidence is convincing that the financial industry has paid think tanks to promote policy that favours the financial industry, not the other 99% of Canadians. Regrettably, because many politicians do not have the time, background or skill to properly analyze complex issues, they listen to think tanks extensively.

In 2017, Konrad Yakabuski of the Globe and Mail, wrote:

“Between 2000 and 2015, representatives from Canada's 10 leading think tanks appeared at least 216 times before parliamentary committees and were cited in the Canadian media almost 60,000 times. It gave them and their research priceless exposure and influence in shaping government policy.”

For comparison, the CPP’s gigantic $400 billion surplus has been cited in the media zero times. Please compare zero to 60,000 on an issue involving almost 3,000 times as much money as the $60 million ArriveCan scandal.

We Canadians proudly think freedom of speech and freedom of press flourish in Canada, much more successfully than in almost every other country. This is not true. Here is why:

No media in Canada, including “our” CBC, will publish any details about the CPP’s surplus and potential to solve many of our problems, especially those of the less fortunate.

Allegedly reputable leftwing organizations like CARP and CANAGE have abandoned seniors and abandoned their alleged mandate, probably thanks to generous “donations” from the financial industry.

Think tanks, the generously paid, biased mouthpiece of the financial industry, can gain huge access and influence with politicians and the media.

Individual leftwing researchers like me represent 99% of Canadians. After presenting the above details to my three MPs and all 334 MPs via email, I have received almost zero response. Moreover, any active professor seeking funding for this type of research would probably be rejected by the university’s administration. Why? Such research would lead to a decline in donations to the university from the financial industry.

The tentacles of the greedy financial industry are ubiquitous. This explains why Ms. Freeland and Mr. Carney claim our capitalist system is rigged to favour the super-rich. And why Mr. Poilievre claims “Our system is broken.” And why Ms. Freeland thinks:

"The super-rich have bankrolled a network of conservative think tanks, elite journals, and mass media outlets to dominate the debate over economic policy."

The Save it for a Rainy Day Argument

Some critics suggest we should leave the CPP’s surplus alone, in case CPP Investments suddenly has poor returns. This scenario is especially unlikely because of the diversification of CPP Investments. They are invested in public equity, private equity, real estate, infrastructure, fixed income and credit, all over the world. If a few investments fail, hundreds of other safe investments will offset this failure. Conversely, most individual investors and smaller Canadian pension funds are only invested in public equities, predominantly Canadian companies. If the stock market declines, these pension funds will decline in virtual lockstep. This suggests a CPP surplus distribution is much less risky than with other pension funds.

Finally, generational equity demands a surplus distribution when the surplus is 25% above target or older members of the fund will be deprived. The CPP’s surplus is now 238% above target.

If Untrue, these Claims Merit Legal Action.

It is essential to highlight that, if I am spreading misinformation, I could potentially face a significant "defamation of character" lawsuit. I am leveling accusations against various organizations and individuals, alleging that they have forsaken their fellow Canadians and fallen drastically short of fulfilling their purported mandate.

Despite making these claims for years, no legal action has transpired. This absence of a legal challenge underscores the accuracy of the above information. Furthermore, a court would likely align with the perspective of 99% of Canadians. Finally, the fallout from an unsuccessful, publicized lawsuit could spell disaster for these implicated individuals and organizations that have likely abandoned millions of Canadians for cash.

Seventeen questions that can only be answered with one word:

BRIBERY

Bribery is an unsavory word that most Canadians connect with third world countries. Even though bribery is often responsible for depriving millions of low-income citizens of billions of dollars in benefits, our media never uses the word. Many think, as I did ten years ago, that large-scale bribery could never happen in Canada. I was wrong.

Consider Ontario’s Premier Ford. After promising to never release Toronto’s surrounding Green Belt land to developers, he did just that, making the developers roughly $8 billion wealthier. Fortunately, unlike the financial industry, he cannot afford to bribe the entire Canadian media to remain silent. The media revealed his corruption and he has since backpedaled.

On April 25, 2024, the Globe and Mail wrote:

“A former SNC-Lavalin executive has been sentenced to 3½ years in prison in connection with a bribery scheme for a bridge repair contract in Montreal, the RCMP say.

A police investigation revealed that SNC-Lavalin executives paid bribes of roughly $2.3-million in order to secure a $128-million contract to repair the Jacques Cartier Bridge deck in the early 2000s.

In 2017, Michel Fournier, former chief executive officer of Federal Bridge Corp., admitted to receiving the bribes through Swiss bank accounts between 1997 and 2004. He was sentenced to 5½ years in prison.”

The financial industry, with its huge resources and 47% of all corporate profit, is much more subtle and hidden in its efforts to conceal the truth about the CPP. Probably even a RCMP investigation would never reveal the millions of dollars changing hands.

Unless someone can provide answers other than “BRIBERY” to the following questions, I am convinced that our greedy financial industry has used bribery to enrich Canada’s wealthiest 1% at the expense of Canada’s less fortunate 99%.

Here are the questions.

Why do Ms. Freeland and Mr. Carney claim our capitalist system is rigged to favour the super-rich? Why did Mr. Poilievre state “Our system is broken. Fire the gatekeepers.”, probably alluding to our Chief Actuary and the President of the CBC?

Why does David Meslin, Canada’s expert on democracy, claim “Our political system has evolved into a sophisticated enabler of mass institutionalized bribery... powerful corporations continue to wield enormous power in our legislatures.”

Why does democracywatch.ca claim "Corporations spend $25 billion annually on their lobbying and promotion efforts."

Any party could win a majority by proposing a $200 billion CPP surplus distribution, with no risk to future pensions, and a $50 billion reduction in our troubling deficit. The benefits for Canadians and Canada would be immense. Why has no politician from any party ever even mentioned the CPP’s surplus? Almost all have become mute when confronted with the CPP’s surplus, their probable ticket to re-election.

Why did two of my MPs, after a half hour presentation, show enthusiasm for a CPP surplus distribution, mentioning their re-election would be a surety if their party proposed it. They “sent the ideas to Ottawa”. Why did they then refuse to respond to me, despite repeated requests.

Why did my third MP, the principled Jane Philpott, after a half hour presentation, respond with “It is those disgraceful lobbyists.”?

The most newsworthy story in years is about the CPP’s surplus and what a surplus distribution could do for Canadians and Canada. Why has our entire Canadian media never published one word regarding the CPP’s $400 billion surplus, which is more than ten times our average annual deficit and almost 3,000 times the size of the ArriveCan scandal.

Why has “our” CBC never mentioned the CPP’s surplus, despite repeated submissions by me?

Why has no think tank member, actuary, journalist or politician provided one reason to NOT distribute the CPP’s surplus?

Pension fund experts recommend every pension fund should have a representative Board of Governors, primarily composed of contributors and pensioners. Such a Board would have declared a surplus distribution years ago. Why does the CPP not have such a Board of Governors?

Almost all government departments are audited by our Auditor General or our CRA. They are our watch dogs who report on scandals like the ArriveCan scandal. The CPP holds 10% of the lifetime earnings of most Canadians, trillions of dollars. Why is our Auditor General or our CRA not allowed to audit the work of our Chief Actuary?

Why have ten top Canadian actuaries all denied the CPP’s obvious surplus with vacuous arguments?

Malcolm Hamilton is a top Canadian actuary who is associated with the think tank C. D. Howe Institute. They will not reveal who funds them. Why did Malcolm spend 40 hours trying to convince me the CPP has no surplus?

Why did one top actuary near retirement, in a moment of conscience, state our Chief Actuary “invents measures that are easily manipulated so that actuaries can control the narrative and hide things at will.”

Why did CARP and CANAGE, Canada’s two best advocates for seniors’ rights, ignore repeated requests to assist in advocating for a CPP surplus distribution, thereby helping deprive six million seniors of a deserved $10,000 each, $60 billion in total.

Generational equity is the goal of all pension fund managers. To achieve generational equity, most pension funds distribute a surplus when it is 25% above target. The CPP’s surplus is now 238% above target. A $10,000 surplus payment to those 100,000 low-income seniors who will die this year could lead to their increased quality of life and their increased longevity. Why are our politicians and the others complicit in this cover-up not guilty of shortening the lives of thousands of innocent, struggling Canadians?

Why did Lifeworks’ actuaries claim Alberta deserves 53% of our CPP fund when the truth is roughly 16%? Why did the Canadian media then unfairly attribute this ridiculous claim to Premier Smith, portraying her as unhinged and unCanadian. She should have been portrayed as the only politician in Canada impervious to bribes and genuinely concerned for the welfare of Albertans.

A summary of this cover-up, now involving $200 billion

Impact, Understanding and Awareness are Gaining Traction.

Given my widespread dissemination of thousands of emails to influential Canadians, including Alberta Premier Danielle Smith, the news of the CPP’s surplus and potential is gaining traction. Recent developments have heightened the mounting evidence surrounding this cover-up:

CPP Investments’ proud claim: Regrettably CPP Investments’ sole mandate is to invest. They are frustrated because benefits from their outstanding investment success are not reaching Canadians. Possibly because of prodding by me, they have published the graph above that shows them as the best pension fund investor in the world. As millions of Canadians realize their hard-earned contributions have been invested so successfully, they will start wondering “Why am I not reaping the benefits of this investment prowess? After all, it was my money they used to create this ‘gigantic’ surplus.”

Financial Industry wealth and ongoing greed: The news that the financial industry, predominantly composed of greedy, male millionaires, claims 47% of all corporate profits in Canada while contributing only 7.4% to our GDP, is slowly reaching many Canadians. To emphasize how disproportionate 47% is, in the US, including unsavory Wall Street, the financial industry earns 17% of all corporate profits.

Females are being abused more than males. Most wealthy members of the financial industry are males. Conversely, two thirds of low-income seniors are females. Moreover, thousands of struggling single mothers are dealing with no support from absent fathers. Women’s groups have been notified. Regrettably, there is little evidence of their taking action.

Politicians may capitulate: With…

an election on the horizon,

all 334 MPs having received these details,

99% of Canadians likely voting for a surplus distribution,

a surplus distribution giving Canadians and Canada immense benefits,

all three parties complicit in remaining silent,

our deficit and debt mushrooming,

our economy sputtering,

seniors dying much earlier than they should,

an ANYONE BUT THE INCUMBENT (See below) policy looming,

and much more,…complicit politicians may soon agree to ignore the bribes and do the right thing.

Will our next Prime Minister act appropriately? Pierre Poilievre, our probable next Prime Minister, is aware of the CPP’s surplus and potential, as evident in his email response.

On May 3, 2024, Mr. Poilievre, stated in an article published in The National Post, entitled,

“Memo to Corporate Canada - fire your lobbyist. Ignore politicians. Go to the people.”

“Obviously, my future government will do exactly the opposite of Trudeau on almost every issue. But that does not mean that businesses will get their way. In fact, they will get nothing from me unless they convince the people first. So here is a how-to guide for dealing with a Poilievre government.

If you do have a policy proposal, don’t tell me about it. Convince Canadians that it’s good for them. Communicate your policy’s benefits directly to workers, consumers and retirees…Your communications must reach truckers, waitresses, nurses, carpenters, - all the people who are to productive to tune into the above-mentioned platforms.”

It appears the days of the lobbyist, in some cases, briber, will be over when Mr. Poilievre is elected. Time will tell. Meanwhile, encouraged by his guidance, I will send these details to common Canadians - the associations that represent workers, consumers, retirees, truckers, waitresses, nurses, carpenters and many more.

M. Poilievre has openly acknowledged that "Our system is broken.", indicating that scandals like this CPP cover-up are commonplace, and he intends to fix things. Additionally, he wants to “Fire the gatekeepers”, probably including our Chief Actuary who has ignored an irrefutable $400 billion CPP surplus.

Finally, he wants to "Defund the CBC." This is justifiable because “our” complicit CBC president, Catherine Tait, has obviously ordered journalists to never mention the CPP’s surplus, probably obeying instructions from Prime Minister Trudeau.

The question remains: If elected as Prime Minister, will Mr. Poilievre ignore all other pressures and give Canada what 99% of Canadians want – CPP reform? Any pressure exerted by Canadian voters now could play a pivotal role in his moving toward CPP reform.

6. Premier Smith’s desire to bring the benefits to Alberta: Premier Smith has received these CPP surplus details. Her recently published Alberta Pension Plan website has promised benefits very similar to the benefits described above. Below are two snapshots from the Alberta Pension Plan website.

Instead of providing Alberta workers with a $10,000 lump sum surplus payment, Alberta would give all employees and contribution-matching employers a $1,425 contribution reduction each, per year.

Her actions have brought the CPP’s surplus to the limelight. With…

Her justifiable desire to withdraw from the CPP,

Ottawa’s refusal to distribute the surplus,

the outlandish actuarial claim that Alberta deserves 53% of the fund,

…it is now much more likely that curious Canadians will investigate and take action. Moreover, other premiers may also soon demand their province’s share of our CPP fund.

7. The association with shortening lives is stark: Those 100,000 low-income seniors who will pass on this year could have each significantly enhanced their quality of life and longevity with their deserved $10,000. Additionally, 1.9 million other low-income seniors could enjoy a hundredfold increase in their cash available after covering rent and day-to-day expenses, using their deserved $10,000. Those complicit in this cover-up are responsible for these shortened lives. They may soon want to renege on their promise of silence.

8. Upcoming exposé: An upcoming book on this entire cover-up will expose many complicit individuals. Because millions of Canadians now deserve $10,000 from the CPP’s surplus, and the book will help them receive it, the book could be a bestseller.

Moreover, stories revealing corruption and bribery typically captivate audiences. The widespread interest and anger against Ontario Premier Ford's blatant corruption is unmistakable.

The book will include a Rogue’s Gallery of all those complicit Canadians who disgracefully abandoned millions of less fortunate Canadians, for cash. Some readers will inspect the Rogue’s Gallery to see if any of their more unsavory acquaintances are publicly shamed. Those complicit in this cover-up will want to see if they have been embarrassingly included.

My personal journey from a naive, trusting Canadian to uncovering possibly the biggest scandal in Canadian history is an interesting tale of rejection, constant lies, doubt, discovery, determination, thousands of unpaid hours and helping bring $440 million more per year to one million low-income seniors.

In response to this upcoming book, the members of the three complicit industries may seek to disentangle themselves before millions of resentful Canadians link them to corruption, bribery and shortening the lives of innocent Canadians.

9. The news is circulating persistently: Because of the lack of publication supplied by mainstream media, the above information has been emailed to thousands of influential Canadians. Many recipients have forwarded these details to thousands of others. My associates and I are in the process of sending thousands more emails to reach as many influential Canadians as we can. Social media could soon make this topic “Go viral.” The void in mainstream media coverage on this topic will soon be replaced with accurate information, instead of no information or misinformation.

10. The impact of complicit Canadians’ participation is coming to light. Many journalists, actuaries, politicians, and investment advisors are well aware of this cover-up. They remain silent because of the potential consequences for combatting it, including job loss, decreased income, blacklisting for future employment, and exile by colleagues. Will some disgruntled, unemployed participants break ranks and join the move to make these cover-up details public? For example, the CBC recently laid off 10% of its journalists. Throughout Canada, employment for journalists is declining at an unprecedented rate. Will one of them soon independently write and publish an article about this cover-up?

11. The impact of complicity is much more than anticipated. Many participants in this cover-up probably did not realize the profound impact their participation is having on Canadians and Canada. It appears that the financial industry said to would-be participants, for example,

“We will ‘donate’ $X million to your organization or political party. All you need to do in return is to never mention the CPP’s surplus.”

Most recipients probably said to themselves “This one condition can’t hurt Canadians much and we badly need funding, so let’s accept it.”

They are gradually learning that they are complicit in robbing Canadians and Canada of huge, deserved benefits. Moreover, they are guilty of shortening the lives of thousands of innocent Canadians every year. Many organizations and individuals are likely now having second thoughts and will not continue participation. These participants are not bank robbers. Many are respected, law-abiding Canadian citizens, with a conscience. For many reasons, they may soon refuse participation in this insidious cover-up.

How can Canadians Combat this Diabolical Cover-up?

Despite this abundance of compelling evidence, you may remain skeptical. You might find it worthwhile to seek explanations from various sources such as your MP, the media, actuaries, think tanks, journalists, as well as organizations like CARP, CANAGE, or any individual or group with potential ties to the financial industry. In doing so, you will experience, like myself, a deafening silence in response.

When the formidable financial, media, and actuarial industries clandestinely collaborate, with possibly $1.25 billion in cash helping, it appears they can destroy democracy. To counteract this cover-up, the collective action of many thousands of Canadians is imperative. Only then will these three complicit industries backpedal and abandon their deceitful efforts.

With all MPs implicated in this alleged collusion, politicians find themselves in a precarious situation. Personally, I have sought explanations via email from all 334 MPs, including those representing my local constituency. Each MP had the opportunity to assert their ethical stance by saying to their leader, "I am ethical, and I will not participate in this." However, none chose to do so. They also could have rallied colleagues and initiated a Private Members Bill to legislate a CPP surplus distribution. Unfortunately, none took these steps. However, when an MP defies his party leader, he risks being ejected from the party, no re-election and a substantially reduced pension.

Consider Jane Philpott and Jodi Wilson-Rayboud. As respected MPs, they showed public dissent over the handling of the SNC-Lavalin affair, a political controversy involving allegations of political interference in a criminal prosecution. Prime Minister Trudeau ejected them from the Liberal caucus for defending democracy instead of obeying his instructions. Is Canada closer to a democracy or a dictatorship?

This CPP surplus cover-up is a glaring failure in democracy. To combat it requires the adoption of extreme measures to ensure that future MPs expose, rather than endorse, any bribery that favors the 1% over the 99%. After all, we live in Canada, not Russia or China.

How you can help: The ANYONE BUT THE INCUMBENT Strategy

Our MPs are elected,

“to represent us in the House of Commons and work on our behalf to create new policies and laws.”

The evidence above is convincing that our MPs have sold us out. Because all three parties remain mute on this crucial topic, we are left with one reasonable option.

Canadians can ask their MP for an explanation of why the CPP’s surplus is being ignored. Without a reasonable explanation, which is inevitable, they can notify their MP that they will vote for ANYONE BUT THE INCUMBENT. Participants in this cover-up might then backpedal for the following reasons:.

Backbenchers’ Demands: Faced with the prospect of not being re-elected, backbenchers may exert pressure on their leaders to propose CPP reform. The threat of unemployment and, for many, a potential million-dollar loss in MP pension benefits makes this demand particularly pressing.

Party Leaders’ Response: Because party leaders rely on their incumbents being re-elected for overall electoral success, party leaders may be compelled to propose CPP reform.

Repercussions for Leaders: If party leaders are perceived as associated with bribery and shortening lives, they may backpedal on their failure to support CPP reform, as corrupt Premier Ford of Ontario has backpedaled on his recent multibillion-dollar corruption scandal.

Three Complicit Industry’s Reaction: Recognizing that the truth is emerging, these complicit industries may release politicians and the media from any existing bribery agreements. They are likely aware that, if millions of Canadians become aware of these details, the potential damage to their personal image and their industry could be significant. Moreover, no Canadian wants to be associated with shortening the lives of innocent Canadians.

On behalf of millions of struggling Canadians, I encourage you to take five minutes and send the following email to your MP, whose email address can be found here:

Dear Sir or Madam,

Based on www.fixthecpp.ca and standard pension practices, our CPP should be distributing $200 billion of its $400 billion surplus to deserving Canadians. Moreover, there are numerous other substantial benefits that could arise from revised CPP legislation. If you cannot provide an explanation as to why your party has refrained from even discussing these potential benefits, I will be voting for anyone but you in the next election.

Sincerely,

[Your Name]”

The Forward this Message Liberally Strategy

As an influential, ethical individual, you've received this information along with a sincere plea to leverage your influence on behalf of millions of less fortunate Canadians. One impactful way to initiate this support is by sharing this email with as many Canadians as possible. These crucial details will never be communicated by our traditional Canadian media, and it's critical that people are aware that the CPP now owes them $10,000 and potentially much more.

If you are an employer: Forward this email to your employees. They may press their MPs for an explanation. Additionally, your business stands to benefit with a potential 20% increase in profit this year, a 5% increase in subsequent years and thankful employees with $10,000 more in their pockets, therefore not seeking a huge pay raise.

If you oversee an association: Forward this information to your members, as the media will not. They deserve to be informed and take action, if they want.

If you are a journalist: Convey to media owners that their continued, selfish refusal to publish the truth about the CPP could result in a deep decline in trust, reduced readership, and diminished advertising revenue, resulting in much fewer employment opportunities for journalists.

If you are an MP: Champion democracy and represent the desires of the 99% of Canadians who elected you. If your leader is unresponsive, consider initiating a Private Members’ Bill.

If you are a provincial or municipal politician: Advocate for democracy by urging your MPs to address this failure to distribute the CPP’s surplus, emphasizing the impact on local neighborhoods. Join Premier Smith of Alberta in fighting the greedy financial industry.

If you are any other Canadian: Share this information with your friends, family, and associates. Many would want to know, could use an extra $10,000, will thank you, and take action themselves.

If you are complicit: Rather than enabling this cover-up, contemplate raising objections to it. Failing to do so may lead to your inclusion in the forthcoming book's Rogue’s Gallery, which will name complicit individuals and organizations. Do you really want to be associated with shortening innocent Canadians' lives?

Why am I so passionate about this topic? I feel guilty. Like almost all public sector employees, I currently enjoy a significant professor's pension, equating to 70% of my final pay and indexed to match inflation. This means my retirement is a joy, not a struggle. Additionally, in 2000, I received an unexpected $20,000 surplus payment from the Ryerson University Pension Plan when it only had an 18% surplus. It's important to note that all Canadians, because of employer matching, contributed to half of these generous public sector pensions, given to roughly 20% of Canadians.

I am deeply offended by the selfish cadre of millionaires who have subtly used their deep pockets to rig our system so that they increase their wealth at the expense of the less fortunate. As a concerned Canadian, I cannot, in good conscience, stand idly by.

There are 51 tax loopholes in Canada. And 47 of them favour the rich. An associate who enjoys an estimated $150,000 income boasts he never pays any income tax, thanks to these loopholes.

Consider this Newsweek story on billionaire Warren Buffett:

“Buffett's wealth grew by $24.3 billion between 2014 and 2018 but he only paid $23.7 million in taxes, a rate of 0.1 percent, after reporting taxable income of $125 million, according to an article published Tuesday by ProPublica.”

Finally, I heartily agree with The Economist:

“The marginal benefit of an extra $1,000 is greater for the poor than the rich. A hungry family might buy food for a month; a banker might blow that amount on a single dinner, not including the wine.”

Likely, millions of struggling Canadians agree. We sincerely hope that you will join this David/Goliath battle. It will only take five minutes to email your MP and could lead to your receiving $10,000.

Finally, if you have any creative ideas on how to further bring CPP justice to Canada, I encourage you to exercise them.

Any comments, suggestions and criticisms are greatly appreciated.

Sincerely,

Ross Macnaughton

Professor emeritus

Ryerson University aka TMU

Possibly the biggest cover-up in Canadian history

The following content has been emailed to hundreds of influential Canadians, starting in November 2023.

The consequences of the following cover-up are profound, with widespread implications for millions of Canadians and the nation as a whole. On behalf of 99% of Canadians, most of whom are currently grappling with significant challenges, I strongly encourage you to continue reading. Millions of these deprived individuals now deserve huge benefits that are not reaching them, resulting in Canada's wealthiest 1% amassing even greater wealth. It will be demonstrated that this situation involves elements of genocide.

Numerous conspiracy theories abound in today's discourse, and most are grounded in mere speculation with scant evidence. However, the theory I present here is substantiated by a wealth of proof accumulated over my seven years of research as a professor emeritus in Business. ChatGPT lists six conditions needed to validate a conspiracy theory – Evidence, Plausibility, Motivation, Expert Opinion, Critical Thinking and Media Accuracy. You will find all six conditions have been met in the following exposé.

To bolster my credibility, it is worth noting that my research and advocacy efforts played a pivotal role in securing an additional $440 million annually in Guaranteed Income Supplement (GIS) payments for low-income seniors. This accomplishment, achieved through the removal of a 76% GIS calwback rate in the March 2019 federal budget, underscores the tangible impact of my work on the lives of vulnerable individuals.

Why the Canada Pension Plan has a huge surplus.

In the current landscape marked by the challenges of COVID, inflation, high interest rates, and more, there is substantial positive news for Canadians. CPP Investments, responsible for investing 10% of the lifetime earnings of most Canadians, has proven itself to be the premier pension fund investor globally. This distinction is evident in their graph provided below from their website, showcasing their exceptional performance.

In 2010, our CPP fund was in perfect balance, able to fund all pensions for 75 years, as long as CPP Investments maintained a 6% return. Thanks to CPP Investments’ 10.9% return, our $576 billion CPP fund now has a $224 billion surplus, as illustrated in the following graph.