Deserved benefits for Canada’s 99%, mostly struggling

Introduction

Over the past ten years, as a Professor Emeritus who taught The Mathematics of Finance, I have studied the Canada Pension Plan (CPP) on behalf of its 22 million contributors and pensioners. During this time I stumbled on disturbing details that raise serious questions about how the CPP is being managed and how its investment gains are being shared.

Canadians are frequently warned of sophisticated scams. Many are victims. Below gives overwhelming evidence showing our financial industry has subtly orchestrated a scam that is costing 20 million Canadians $10,000 each, on average. The industry now corners 47% of all Canadian corporate profit and is packed with thousands of millionaires. They want to keep earning millions while depriving 99% of Canadians, most struggling, of hundreds of billions of deserved dollars. The evidence follows.

The CPP is important. Most Canadians have contributed 10% of their lifetime earnings to the CPP, trillions of dollars in total. However, no one is appropriately overseeing these contributions on their behalf. Moreover, Albertans are considering separation from Canada based on the CPP injustice described below.

The CPP is not a social program like Old Age Security (OAS) and the Guaranteed Income Supplement (GIS). They both grant money to seniors based on their income level. The CPP is different, If, for example, we are the same age and you contributed double what I contributed every year that we worked, you would receive double the CPP pension that I would receive. This is how all Defined Benefit pension plans operate.

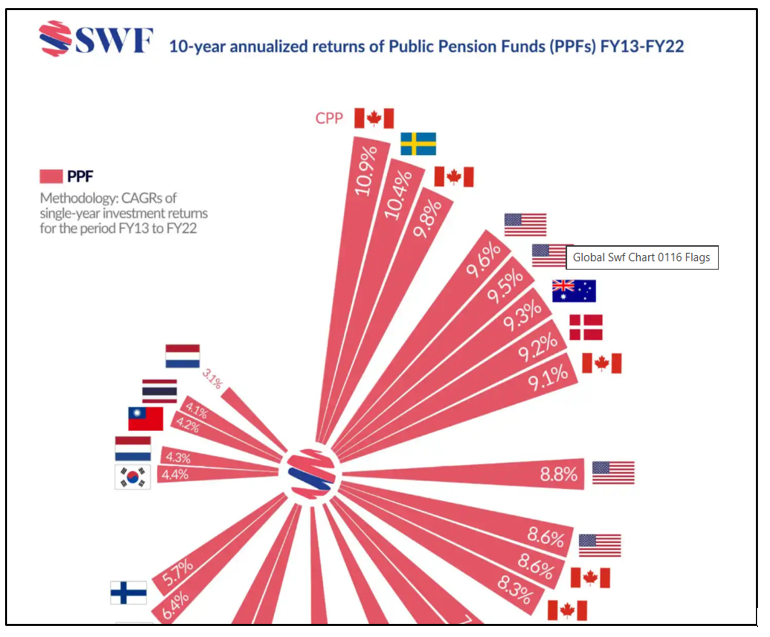

For the past 15 years, CPP Investments’ has been the best pension fund investor in the world, averaging a 10% return when only a 6% return is necessary to meet all pension commitments.

Global SWF, a New York-based pension industry specialist ranked CPP Investments as the best investor of 300 pension funds worldwide

CPP Investments’ outstanding performance has created roughly $500 billion in additional wealth beyond earlier projections. Yet millions of Canadians struggling with rising costs of living have seen no benefit from these gains.

If the recommendations below were implemented, millions of floundering Canadians would enjoy a considerable, deserved improvement in their quality of life. However, the overwhelming evidence indicates the selfish interests of Canada’s wealthiest 1% have been favoured over the interests of the other 99%. On this crucial issue, democracy, freedom of press and actuarial science have all been replaced with a deception that is having a profound negative impact on millions of Canadians and our sputtering economy.

The issue goes far beyond pensions. It affects:

the disposable income available to younger Canadians,

the financial security of seniors,

the strength of Canada’s economy.

Albertans’ desire to separate from Canada.

My interest in the CPP is also partly personal. The MacNaughton family has long been connected to the history of the Canada Pension Plan.

Because CPP Investments has been the best pension fund investor in the world for 15 years, our CPP fund now has a $500 billion surplus as shown here. Fifteen years ago, our Chief Actuary specified a 6% return is necessary for fund stability, resulting in a $366 fund value today. Because CPP Investments has averaged a 10% return for 15 years, our comparable CPP Fund’s value is $725 billion. With an ongoing 10% return, which is likely, the CPP fund only needs roughly $245 billion in the fund to meet all pension commitments. This means our CPP fund now has a $500 billion surplus, 200% above what is needed.

How likely is an ongoing 10% return? Because CPP Investments:

has roughly 2,000 employees with an average income of $575,000 each, with most holding a MBA degree,

has hundreds of employees searching worldwide for profitable private equity investments,

has the resources to purchase a majority share in most small to medium companies, then controlling management using proven expertise,

can also invest in profitable real estate and infrastructure,

can also invest in public equities and fixed income, essentially the only investment options for the average Canadian, aside from a home…

…CPP Investments will likely continue achieving their outstanding 10% return of the last 15 years.

My father’s cousin, Charles MacNaughton, served as Treasurer of Ontario from 1958 to 1962. Representing Canada’s largest province at the time, he was substantially involved in the discussions that shaped the framework of the CPP in its early years.

His son, John MacNaughton—my second cousin—later played a major role in transforming how the CPP invests its funds. After the landmark pension reforms of 1997, John became the first President and CEO of the Canada Pension Plan Investment Board, now known as CPP Investments. Before those reforms, CPP contributions were invested mainly in fixed-income securities. Under his leadership, CPP Investments began investing globally in public equity, private equity, infrastructure, real estate, and more. Over the past fifteen years, this strategy has produced the strongest investment results of all the pension funds in the world.

The purpose of this website is simple: to present the evidence clearly and allow Canadians to judge for themselves.

A big discrepancy in income

With CPP reform, 99% of Canadians would win but Canada’s financial industry would lose

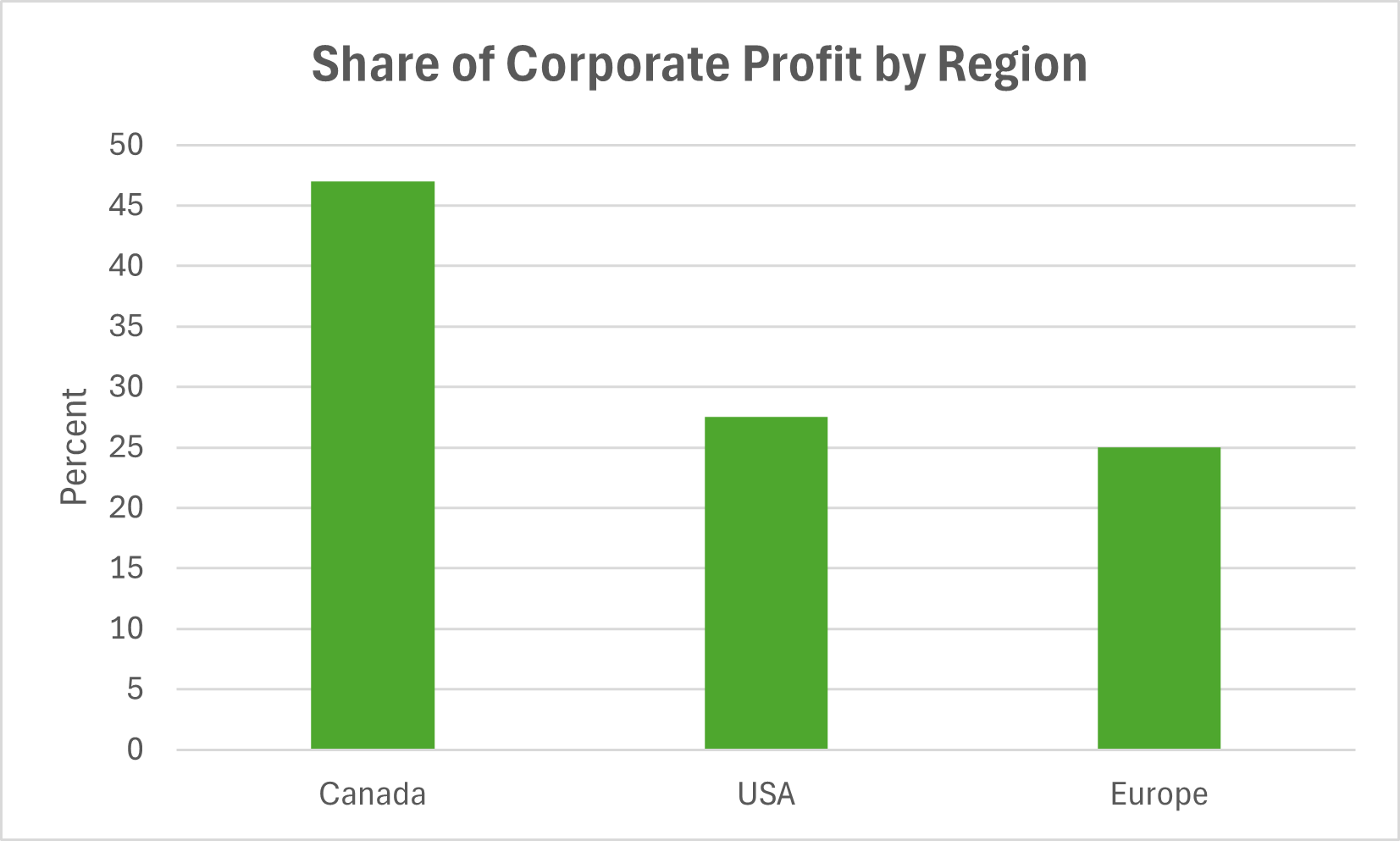

Canada’s financial industry corners 47% of all corporate profit in Canada but only contributes 7.4% to our GDP. For comparison, the US financial industry only collects 25-30% of all corporate profit. Europe’s average is 20-30%.

The Canadian financial industry is awash in cash. In December 2025, the Globe and Mail reported that Canada’s big banks distributed $27.3 billion in bonuses. An estimated 15,000 bank employees received $1.8 million each on top of their salaries.

Meanwhile, millions of Canadians are struggling.

A recent study found that 43% of Canadians are within $200 of insolvency. On March 9, 2026, The Globe and Mail wrote that “Household debt in Canada as a percentage of GDP is 103 per cent, second-highest among 34 OECD countries.”

Another study indicates “54% of Canadians currently have credit card debt, with 72% of Millennials (ages 29-44) carrying such debt.” The credit card interest rate is roughly 20%.

Food bank usage has doubled since 2019.

In Ontario, for example, mortgage delinquency rates are up by 135.2 per cent.

Canada’s ranking in the World Happiness Report plummeted from sixth place in life-satisfaction standings ten years ago to 25th place today, the worst ever. When only Canadians under 25 were counted, Canada fell to 71st. Notably, Finland is ranked number one. Finland’s financial industry earns 18% of all corporate profit compared to Canada’s 47%.

Young Canadians are struggling with mental health. Greenshield research confirms this.

“TORONTO, Nov. 19, 2025 /CNW/ - A new survey from GreenShield, Canada's only national non-profit health care and insurance organization, conducted in partnership with Mental Health Research Canada (MHRC), reveals that over 80% of Canadian youth are overwhelmed by stress and anxiety about their future. Economic pressures – including job insecurity and the rising cost of living – are key drivers.”

Millions of struggling Canadians could gain huge benefits from the CPP’s surplus and potential. If they were aware that the CPP now has a $500 billion surplus and CPP Investments will likely continue investing with a 10% return, they could benefit in three ways.

Benefit # 1 - Voluntary Contributions to CPP Investments

In 2011, when CPP Investments had averaged a modest 5.9% annual returns for ten years, Finance Minister Jim Flaherty researched the possibility of letting Canadians voluntarily invest with CPP Investments. Documents obtained through Access to Information requests indicate that the financial industry strongly opposed the idea, arguing that many Canadians would find it “too confusing.”

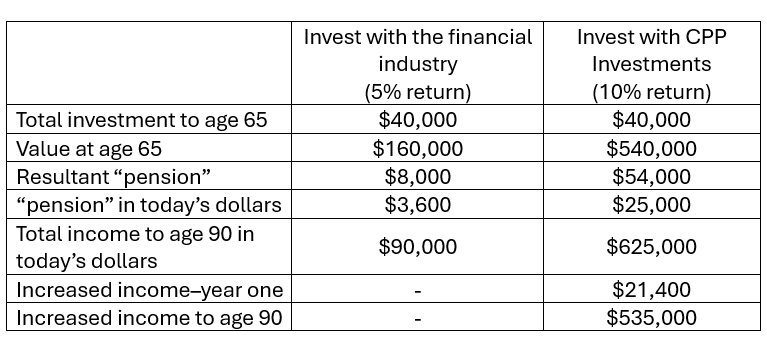

The power of this idea becomes clearer when we consider the effect of compound interest. Albert Einstein once stated, “Compound interest is the eighth wonder of the world.” Consider a simple example. Suppose a 25-year-old Canadian voluntarily invested $1,000 per year with CPP Investments. By retirement at age 65, the total contribution would be $40,000. The following table summarizes the amazing impact.

Consider a 25-year-old Canadian who can afford to invest just $1,000 per year. Should it be with the financial industry, which, based on history, would likely give him a 5% return? Or should it be with CPP Investments which, based on history, would likely give give him a 10% return. The table below compares the two options.

The table shows that, by investing $1,000 per year to age 65 with CPP Investments, instead of the financial industry, a 25-year-old will have $535,000 more in retirement, in today’s dollars, all tax-free.

Because the investor would use a TFSA, there would be zero tax on his entire $625,000 in income. If, for example, in retirement, he had a $50,000 income from other sources, an additional $25,000 would cost him $6,700 per year or $168,000 in total, in additional taxes to age 90.

Consider the impact on our deficit. Two million of six million seniors now live near the poverty line of roughly $25,000 per year. Much of that $25,000 is from GIS payments, increasing our deficit by $17 billion per year. This expense could be mostly, and the struggling that goes with a low income in retirement, would be mostly eliminated.

Moreover, OAS payments, now increasing our deficit by roughly $70 billion per year, would be substantially reduced.

The above analysis presumes a 2% inflation rate and Canadians living, on average, to age 90 in 2066.

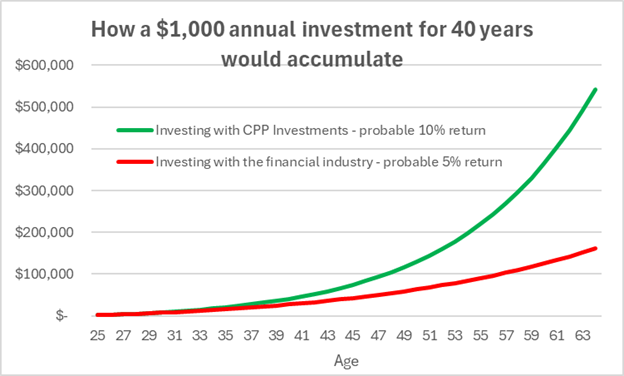

The graph below shows how the two investments would accumulate.

There is another way of illustrating the power of compound interest, when it is combined with CPP investments’ likely 10% return. Presume a 25-year-old wants a $100,000 per year income at age 65, equivalent to a $45,000 income in 2026 dollars. With voluntary contributions, he will need to contribute $1,850 per year. Investing with the financial industry, presuming a typical 5% return, he will need to invest $12,400 per year, almost seven times a much.

Such a change could have important implications for Canada’s financial sector, particularly for wealth-management businesses that earn substantial revenues from managing individual retirement savings. They could eventually lose billions of dollars per year, in investment fee revenue.

Any voluntary investment program would likely require reasonable limits. CPP Investments is designed to manage the assets of the Canada Pension Plan, and absorbing extremely large additional inflows could make it more difficult to deploy capital efficiently. For that reason, policymakers might consider placing an annual cap on voluntary contributions—for example, allowing Canadians to invest up to $1,000 per year through CPP Investments.

This legislation would help neutralize Canada’s mushrooming income inequality.

Benefit #2 - Make the CPP a DC pension plan instead of a DB pension plan

The CPP is a Defined Benefit (DB) pension plan. Your pension is defined, regardless of how well CPP Investments invests your contributions. What is wrong with a CPP DB pension plan? For 10 years, 22 million Canadians have not benefitted from the investment prowess of CPP Investments, which has accumulated a $500 billion surplus, roughly a $23,000 surplus, on average, for every CPP member. Based on standard pension practice, Canadians should be receiving some of this giant surplus. However, our Chief Actuary has, probably for self-serving reasons, ignored millions of struggling Canadians and denied the existence of this $500 billion surplus.

With the current CPP DB plan, Canadians are receiving roughly a 4.75% return on their contributions while CPP Investments is achieving a 10% return, using your money to invest.

The CPP could easily become a Defined Contribution (DC) pension plan. With DC plans, the contributor receives the same return on investment that the investor achieves.

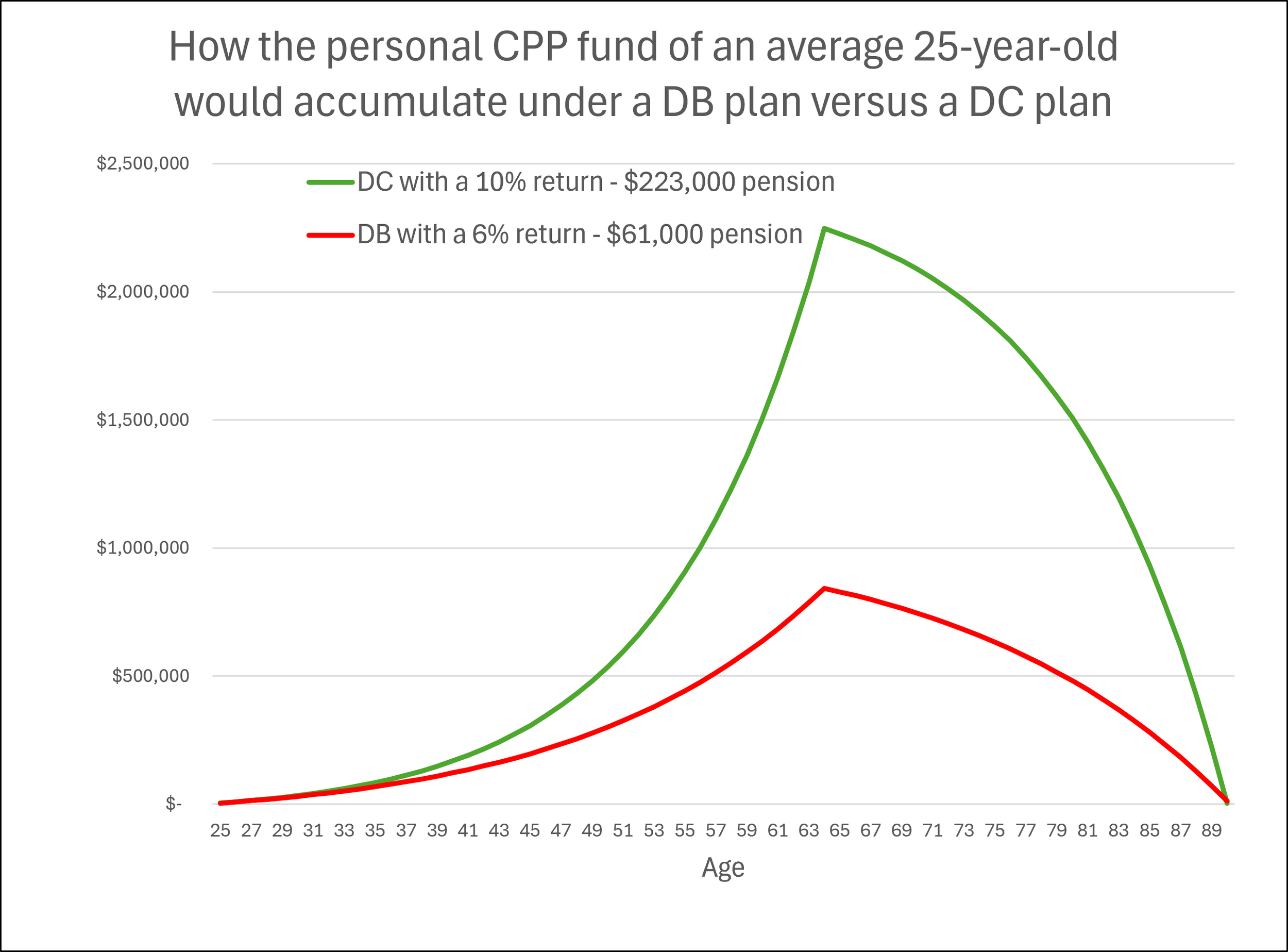

Contributors to the CPP contribute, on average, $5,270 per year when we include employer matching on their behalf. With the current DB plan, in 40 years, an average 25-year-old will receive a pension of $61,000 per year, equivalent to a $28,000 CPP pension in today’s dollars, presuming a 2% inflation rate.

If the CPP became a DC plan, an average 25-year-old would receive an annual income of $223,000 per year, equivalent to a $102,000 income in today’s dollars.

Those Canadians earning $74,600 today and therefore contributing the $8,470 maximum could expect a $163,000 annual income in today’s dollars.

The following graph shows how the personal CPP fund of an average 25-year-old would accumulate under a DB plan versus a DC plan.

This analysis reasonably presumes that, in 40 years, the average Canadian will live to age 90.

Each plan has pros and cons. With a DB plan, pensioners living past 90 will continue to receive their pension. However, if they die before 90, their leftover contributions will be given to pensioners living over 90. Their surviving spouse will receive 60% of their pension up to the CPP maximum.

With a DC plan, those who anticipate living past 90 should withdraw slightly less than their $102,000 each year.

This analysis presumes an ongoing 10% return. If the average return over 40 years, is, for example, 9% or 11%, pensioners should adjust appropriately. The CPP should annually notify them of their portfolio status.

When the DC pensioner passes, whatever remains in the fund will go to his estate. If, for example, he passes at age 85, presuming a 10% return and normal withdrawals, his estate will receive $450,000 in today’s dollars.

Almost all pension plans in the private sector have switched from a DB format to a DC format. This is because DB plans involve risk for the employer. Retirees could live longer than expected. Investments could perform poorly. Failure to meet pension promises could result in devastating publicity for the employer. And the plan would need expensive staffing to monitor investments. The employer would be responsible for all these costs.

With DC plans, the employer simply contributes to the employee’s portfolio, usually matching the employee’s contribution of, for example, 5% of his salary. The employee bears the entire risk. He is often given several investment options by the employer but no guarantees. If the contributions only achieve a 1% return, it is the employee’s loss. If the contributions receive a 10% return, it is the employee’s gain.

However, private sector DC plans have high overheads of 0.5% to 2% annually, resulting in a estimated net return to the investor of roughly 4%. Meanwhile, CPP Investments has averaged a 10% net return for 15 years. The difference is profound. For example, investing $100,000 for 40 years at 4% yields $480,000. Investing $100,000 for 40 years at 10% yields $4.5 million, almost ten times as much.

In 2022, CPP Investments was rated as the best pension fund investor in the world when compared to 300 other pension fund investors. This means that, out of 300 pension funds worldwide, if the CPP became DC, CPP members would be exposed to less risk than all 300 other pension plans, if they converted.

What is the downside of a CPP DC format. After 15 years averaging a 10% return, CPP Investments could average below the CPP’s 6% return target for several years? Even in the unlikely event that it did, government could legislate a contribution increase to offset these low returns.

What is the upside of converting the CPP to a DC format - an estimated 3.6 times the pension, a $102,000 CPP pension in today’s dollars. And if CPP Investments averaged better than a 10% return, millions of Canadians would start to feel like they each won the lottery.

If the CPP switched from a DB to a DC format, as all private sector pension plans have, Canadians would likely enjoy 3.6 times the CPP pension. The downside risk would be virtually zero and the upside benefit could be like winning the lottery.

Broader implications

If the CPP matched Canada’s private sector and switched from a DB to a DC format, the impact on Canada’s financial industry and actuarial profession would be significant.

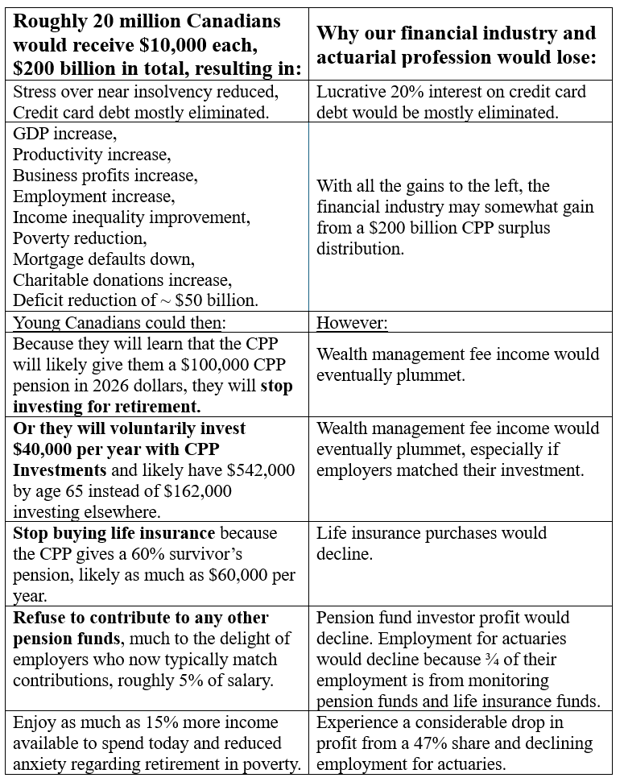

If young Canadians knew that their CPP contributions could probably generate a $102,000 CPP pension in today’s dollars, many would:

Stop investing the recommended 15% of their income towards retirement,

Stop contributing to all other pension plans,

Stop purchasing life insurance because the CPP pays a 60% survivor pension—worth ~$60,000 per year in 2026 dollars.

Demand the ability to voluntarily contribute to CPP Investments, as explained above.

The financial industry would then experience a multibillion-dollar reduction in profit from investment management fees from individuals, pension funds, and life insurance funds. And actuaries, who receive an estimated two thirds of their income from monitoring pension funds and life insurance funds, would experience a considerable decline in employment.

The evidence is overwhelming. The financial industry and actuarial profession have intentionally suppressed the news of the CPP’s surplus and potential so that they can continue to earn multimillion dollar incomes. Consequently, millions of younger Canadians, already disadvantaged and struggling, are being denied a transformative solution to their financial woes.

Currently, the CPP tells Canadians nothing about the status of their personal CPP fund. With a DC format, Canadians could be easily given an annual report of their contribution’s status. For example, they could be told annually,

“As of December 31, 20??, you had contributed $100,000 to the CPP. Thanks to CPP Investments’ 10% return average, your portfolio is now worth $200,000. If you keep contributing as you have, and CPP Investments continues with a likely 10% return, at age 65, you will have a $100,000 CPP pension in today’s dollars.”

If this report indicated CPP Investments was substantially underperforming, then young Canadians could take heed and invest towards retirement.

There are other benefits derived from a CPP DC format. In 2026, benefits for seniors, excluding the CPP, totalled $89 billion per year. Roughly one of every six dollars spent by the government is spent on benefits for seniors. These costs are increasing at a pace much higher than inflation. If most seniors eventually received a $102,000 CPP pension in 2026 dollars, seniors’ mushrooming benefit costs, in the form of the Guaranteed Income Supplement (GIS) and Old Age Security, would decline substantially.

What about seniors’ quality of life? Currently two million of six million seniors barely exist, struggling near the poverty line of roughly $25,000 per year. Changing the CPP from a DB to a DC format could reduce that number considerably. Eventually, with a CPP DC format, almost all two million seniors, with a much larger pension, would live a longer life with improved quality.

(As the author collects his large professor’s pension, half paid for by all Canadians, his quality of life as a senior would decline from an 9 out of 10 to a 2 out of 10 if he tried to exist on $25,000 per year.)

What about younger Canadians? Financial anxiety among young Canadians is increasing rapidly. Impossible house prices, high rents, unemployment, low-paying jobs and the threat of a retirement in poverty are all contributing. If young Canadians were not only told a $100,000 CPP pension is likely, but they could have as much as 15% more income available today, their anxiety would decline substantially.

Canadians under 25 are now ranked 71st on The World Happiness Index. The prospect of a retirement with a middle to upper income and no need to invest today towards retirement would boost that dismal ranking substantially. Young Canadians could receive a message of

Thanks to a Defined Contribution CPP pension, Canada has your back

instead of the current message,

Politicians are ignoring a simple solution to youth unhappiness so that millionaires can become even wealthier.

Summary:

If the CPP became a DC pension plan:

Young Canadians can expect a likely $100,000 pension in 2026 dollars,

The number of low-income seniors would eventually plummet,

GIS and OAS soaring costs would decline,

Young Canadians would have as much as 15% more income to spend today,

Anxiety among young Canadians would decline.

Why is this not happening?

The financial industry would lose billions of dollars in profit, per year,

Employment for actuaries would plummet.

The evidence is considerable that the financial industry, actuarial profession and mainstream media have colluded to prevent this possibility by suppressing the news of the CPP’s surplus and potential.

Benefit # 3 - The CPP’s surplus - help for millions of Canadians who need immediate assistance

Recall that 43% of Canadians are within $200 of insolvency, 54% have credit card debt and the CPP has a 200% surplus. If our Chief Actuary followed standard pension practice and the principle of generational equity, he could, with no risk to future pensions, distribute some of the CPP’s $500 billion surplus.

For example, a $200 billion distribution from the fund would provide roughly $10,000, on average, to about 20 million Canadians, most struggling.

Such a distribution would have have broad economic effects. Additional income in the hands of millions of households would increase spending throughout the economy, supporting improvements in:

debt relief for 43% of Canadians

income inequality

employment

GDP growth

productivity

business profits

poverty reduction

charitable giving

Almost all social programs that help struggling Canadians increase our deficit. A $200 billion CPP surplus distribution would decrease our mushrooming deficit by an estimated $50 billion, through increased income tax, increased HST and reduced social programs.

The Impact is Devastating on Millions of Struggling Canadians, Especially Seniors

The Canadian Anti-Fraud Centre’s 2024 report says people aged 60+ accounted for 40.3% of all reported dollar losses. Imagine, for example, a scammer convinced a struggling, confused low-income senior to e-transfer him $1,000. Most Canadians would recommend considerable jail time for such a thief.

Meanwhile, the failure to follow standard pension practice and distribute any pension fund surplus that is 25% above target means two million low-income seniors are not receiving a deserved $20 billion in total, $10,000 each, on average. This means the self-serving perpetrators of this CPP-surplus-denial scam are responsible for depriving low-income seniors of 20 million times the $1,000 that the example scammer stole. Where is their jail time?

Since 2016, one million low-income seniors have died, never receiving their deserved $10,000 from the CPP’s surplus. Studies show that those in the top quintile of earnings live 13 years longer than those in the bottom quintile. Many of these low-income seniors could have led a longer life with increased quality if they had received their $10,000 from the CPP’s surplus, a 40% increase in income.

Suppressing the news of the CPP’s $500 billion surplus is a national disgrace. On behalf of those 100,000 seniors who will continue dying every year, it needs to be asked. Why are the greedy perpetrators not guilty of genocide?

Who, how and why is explained below. In a country that Canadians think is reasonably democratic, the overwhelming evidence points to cover-up that dwarfs the findings of the Charbonneau Commission, where hundreds of politicians, bureaucrats and consultants colluded to profit handsomely from inflating infrastructure costs in Quebec by 25%.

Women, Income Inequality, and the Fight for Financial Fairness in Canada

Women are disproportionately affected by the outcomes of systems that remain largely shaped by male-dominated leadership.

Approximately two-thirds of low-income seniors are women. During their working years, women earn, on average, about 87 cents for every dollar earned by men, resulting in lower lifetime savings and reduced retirement security. When families separate, women most often assume primary responsibility for childcare, frequently bearing the financial strain that follows. In some cases, support payments are inconsistent or absent, leaving mothers to pursue costly legal remedies—or to manage alone.

At the same time, women remain underrepresented in many of the institutions that influence financial outcomes. Only about 25–30% of senior roles in the financial industry are held by women. In the actuarial profession, women represent roughly one-third of practitioners, with fewer at senior levels. In media leadership, women also account for only about one-quarter to one-third of decision-making positions.

The result is a gap not only in income, but in influence—particularly in areas that shape financial policy, retirement systems, and public awareness.

If you are a woman, your voice is essential in addressing these issues and advocating for fairer outcomes. And if you believe in equity and accountability, I encourage you—regardless of gender—to support efforts that seek meaningful change.

The only senior politician willing to combat this cover-up on behalf of her constituents is a woman, Premier Smith.

A summary of the pros and cons of these recommendations

The benefits summarized in the left column would bring a huge improvement to the lives of millions of struggling Canadians and Canada’s anemic economy.

How Canada Could Rise in the Happiness Rankings

In The World Happiness Report, while Canada has plummeted from a ranking of 25 from 6, Finland consistently ranks first. Finland’s society is built on:

very low levels of corruption,

high trust in government and public institutions,

a strong social safety net,

low income inequality.

These factors create a sense of stability and security that underpins overall well-being.

Younger generations face a wide range of challenges: high housing costs, rising rents, growing income inequality, climate concerns, and increasing financial stress.

Demographic trends also highlight the economic challenges facing younger generations. Since the mid-1970s, Canada’s fertility rate has declined significantly—from about 2.1 children per woman, the level needed to sustain population growth, to roughly 1.25 today. To deprive Canada’s struggling youth of these multi-billion dollar CPP benefits so that the executives in the financial industry can increase their millionaire wealth is criminal. However, legally, the perpetrators of this subtle cover-up probably enjoy complete protection.

Recall that Canada’s under-25 population is so unhappy that, in 2026, Canada is ranked 71st in The World Happiness Report for that age group. With 70 nations ranking above us, who must be near us or below us in the ranking? Likely, only nations rife with poverty, suffering, low income and half our longevity.

Imagine how much happier our younger Canadians would be if our politicians told them the truth:

you can expect a likely $100,000 CPP pension in 2026 dollars,

you don’t need to invest anything today towards retirement,

you don’t need to buy life insurance,

you can make triple the money by investing voluntarily with CPP Investments instead of the financial industry,

you don’t need to contribute to any other pension funds.

Currently, they likely have a sense that the system is failing them and older Canadians are thriving at their expense. And there is nothing they can do about it.

To be fair, a big reason for youth unhappiness is unemployment. However, if the CPP followed standard pension practice and released a deserved $200 billion surplus payment, roughly $10,000 to each of 20 million Canadians, the resultant spending would create thousands of jobs. And if young Canadians were told they no longer needed to invest towards retirement, their extra income available today would also stimulate spending and also create many thousands of jobs.

If our legislators were to adopt the CPP legislation described above, Canada could significantly improve its standing in TheWorld Happiness Report rankings. More importantly, it would enhance the day-to-day lives of millions of Canadians, now struggling.

Is there nothing young Canadians can do about it? What about Generation Squeeze, probably Canada’s largest organization dedicated to helping young Canadians. It allegedly:

“cuts through political noise to hold governments accountable to young and future generations. We're a breath of fresh credibility and academic rigour in an era of misinformation.”

Regarding funding, their website states:

“Gen Squeeze research and policy judgments are made independently, and not on the basis of donor or funder support. These judgements are guided by the best available evidence, and the expertise of our network of research alliances, partners and volunteers.”

Professor Paul Kershaw of UBC is the leader. I have repeatedly presented him with the above details. He has provided absolutely zero defence of his inaction regarding such a crucial topic. If he used his considerable pipeline to educate thousands of young Canadians regarding the CPP’s surplus and potential, it might generate a groundswell of protest. Thousands of young Canadians might protest so strongly that our government and media would be forced to pay attention. Such a protest could even “go viral”.

However, Professor Kershaw acts like leaders of numerous other allegedly benevolent organizations across Canada. Generation Squeeze has probably received a considerable annual donation from the financial industry as long as they remain silent regarding the CPP’s surplus and potential. If Professor Kershaw acted appropriately, we could likely bring Canada’s under-25 population from a disgusting ranking of 71 on The World happiness Report back to a reasonable ranking of 6, what Canada, overall, was in 2016.

Professor Kershaw belongs high on The Reverse Order of Canada List. First, he masqueraded as the prime watchdog and advocate for Canada’s struggling youth, thereby making millions of young Canadians conclude that, with all those resources and funding, “He has probably uncovered and advocated against any and all injustice against Canada’s young.” Then, when given overwhelming evidence of a cover-up that is depriving millions of young Canadians of benefits in the hundreds of billions of dollars, he has remained disgracefully silent. It should be noted that, if my research is incorrect, I could face a lawsuit.

A pathetic defence from Finance Minister Freeland

On Sept. 11, 2024, Finance Minister Freeland defended her inaction on this crucial issue. In an email to me, she stated:

“Consequently, the large build-up in the CPP Fund is necessary to pay for the promised level of benefits, in particular to the large baby boom generation.

In addition, it is important to maintain a certain buffer in the CPP Fund to protect against sudden and unexpected negative shocks to the global economy, such as a collapse of oil prices, a financial crisis or the impact of a global pandemic on the world economy. “

Her response is sadly lacking. Firstly, actuaries have already planned for “our large baby boom generation.” Secondly, the pension fund surplus guideline “to protect against sudden and unexpected negative shocks to the global economy” is a 25% surplus. The CPP now has a 200% surplus.

This overzealous caution is absurd. It is akin to a multi-millionaire saying,

“I am only spending $5 for lunch at McDonald’s because my multimillion-dollar portfolio could plummet in value tomorrow. And my will says that my children and grandchildren, now going to food banks, will receive nothing until ten years after I die.”

Why aren’t these benefits reaching millions of struggling Canadians?

Three powerful, influential industries or professions would lose billions of dollars and lucrative employment if the news of the CPP’s surplus becomes known. The evidence, collected over ten years, that they have orchestrated a massive cover-up, can be found by clicking: